What are taxable entities?

The term ‘taxable entity’ refers to an individual or a business that must file a tax return and pay income tax on earnings. Individuals and corporations are both subject to income tax and are both considered taxable entities.

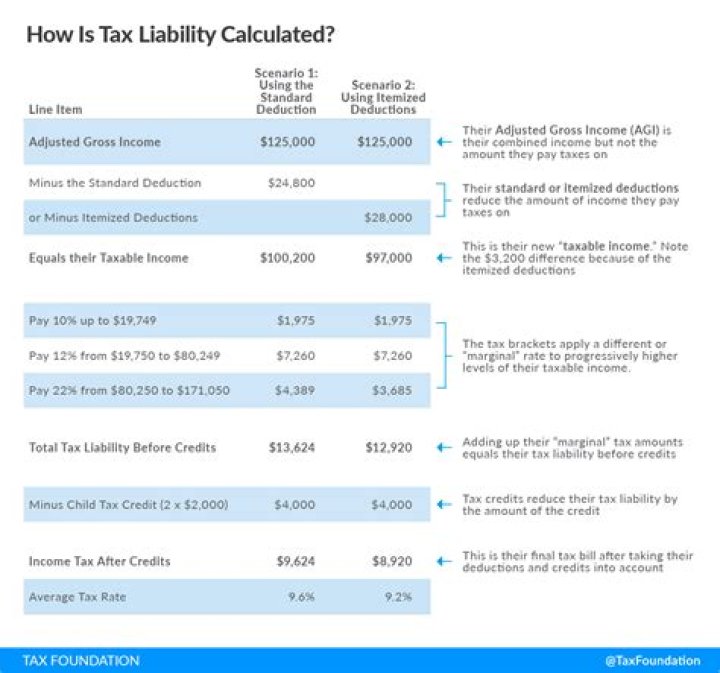

What are the three entities that are taxed by the CRA?

Personal, business, corporation, and trust income tax.

Is Cerb counted as income?

If you received Canada Emergency Response Benefit (CERB) from Service Canada or any Employment Insurance (EI) benefit payments, you should get a T4E tax slip with the amounts you received. These benefit amounts are taxable income.

According to the Code, individuals, most corporations, and fiduciaries (estates and trusts) are taxable entities. Other entities, such as sole proprietorships, part- nerships, and so-called ”S” corporations, are not required to pay tax on any taxable income they might have.

Is it mandatory for tax officer to use e-proceeding facility?

As part of e-governance initiative to facilitate conduct of assessment proceedings electronically, Income-tax Dept. has launched ‘E-Proceeding’ facility. Under this initiative, CBDT has made it mandatory for the tax officers to take recourse of electronic communications for all limited and complete scrutiny.

When do you pay taxes to a flow through entity?

Also known as a “flow-through entity” or “fiscally transparent entity,” this means that the business itself pays no taxes. Instead, taxes are “passed through” to the owner, who pays them in their personal returns under ordinary income tax rates on the typical Tax Day, usually April 15 (July 15 in 2020).

Why do I need a foreign entity W-8 form?

These forms are a direct result of government regulations associated with the Foreign Account Tax Compliance Act (FATCA).

Can a country Z de register as a separate entity?

The Country Z DE will register as an entity separate from its owner, in order to be treated as a reporting Model 1 FFI, and will receive its own GIIN. Updated 8-25-15: Q3 has been updated to clarify that, unless a specified exception applies, a branch must register as a branch of its owner and not as a separate entity.