What are the 3 types of taxes and how do they differ?

Tax systems in the U.S. fall into three main categories: Regressive, proportional, and progressive. Regressive taxes have a greater impact on lower-income individuals than the wealthy. Proportional tax, also referred to as a flat tax, affects low-, middle-, and high-income earners relatively equally.

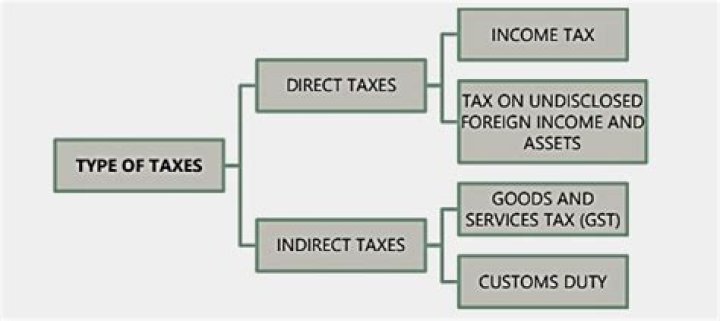

How are most taxes classified?

Taxes are most commonly classified as either direct or indirect, an example of the former type being the income tax and of the latter the sales tax. It is usually said that a direct tax is one that cannot be shifted by the taxpayer to someone else, whereas an indirect tax can be.

What are the 4 types of taxes we are subject to?

Learn about 12 specific taxes, four within each main category—earn: individual income taxes, corporate income taxes, payroll taxes, and capital gains taxes; buy: sales taxes, gross receipts taxes, value-added taxes, and excise taxes; and own: property taxes, tangible personal property taxes, estate and inheritance …

What is classified as tax evasion?

Tax evasion is an illegal activity in which a person or entity deliberately avoids paying a true tax liability. Those caught evading taxes are generally subject to criminal charges and substantial penalties. To willfully fail to pay taxes is a federal offense under the Internal Revenue Service (IRS) tax code.

What are the different types of Tax Court opinions?

The Tax Court issues two categories of opinions: (1) formally published dispositions; and (2) unpublished dispositions.

How are Tax Court opinions binding and precedential?

T.C. opinions are binding, precedential, and published by the Tax Court. They generally address issues of first impression, issues that impact a large number of taxpayers, or matters related to the validity or invalidity of regulations.

Can a taxpayer cite a Tax Court opinion?

However, similar to summary opinions, there is no express rule prohibiting the citation to orders. Thus, if any issues has never been addressed by the Tax Court in an opinion, but has been discussed in an order, taxpayers may want to bring the order to the Court attention.

Are there more memo opinions or t.c.opinions?

This reflects the fact that there are significantly more memo opinions than T.C. opinions each year (approximately 90 percent of all Tax Court opinions are memo opinions), providing taxpayers with more authority upon which to provide support for their position.