What are the differences between the cash basis of accounting and the accrual basis of accounting?

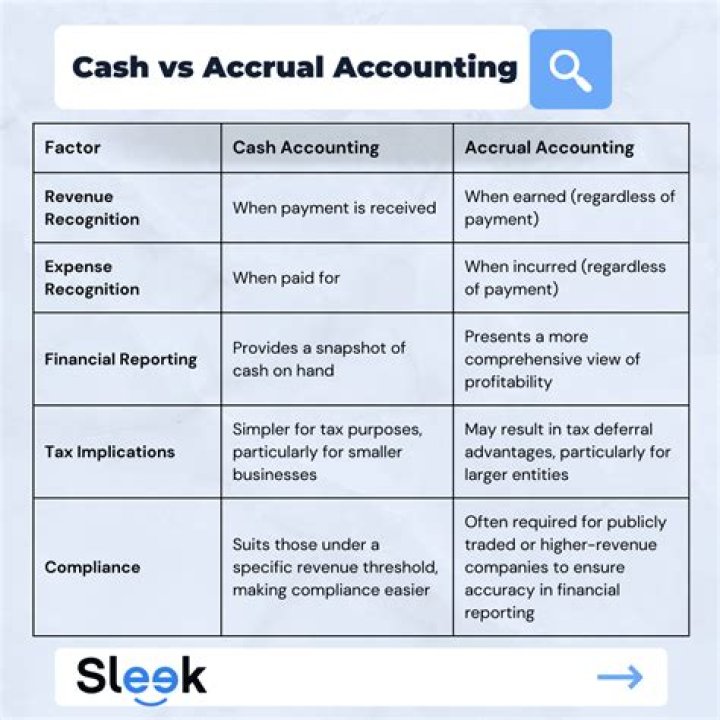

The difference between cash and accrual accounting lies in the timing of when sales and purchases are recorded in your accounts. Cash accounting recognizes revenue and expenses only when money changes hands, but accrual accounting recognizes revenue when it’s earned, and expenses when they’re billed (but not paid).

Which is more confusing accrual basis or cash basis accounting?

Unlike the cash method, the accrual method makes it more difficult to get a clear picture of cash flows due to the timing of receipts from customers and payments to suppliers. The cash flow statement is very important to read and understand when you are operating your books on the accrual method.

Who can use the cash-basis of accounting?

Revenue procedure 2000-22 allows any company that meets a sales test to use the cash method of accounting for tax purposes. This includes sole proprietors, partnerships, S corporations and regular corporations.

Why cash-basis accounting is bad?

The disadvantages of cash-basis accounting: It can be misleading because it may show that you are profitable when you simply haven’t paid your bills yet. It is unhelpful when it comes to making business decisions because you only have a day-to-day view of your finances, rather than a long-term perspective.

Is cash basis accounting illegal?

The same concept applies to making purchases on credit. If your expenses are made on credit, you can’t use cash-basis accounting. With cash-basis accounting, you do not record expenses that you will pay in the future but have not yet paid. The IRS restricts some businesses from using the cash-basis method.

Can I switch from accrual to cash basis?

If you want to change from using the accrual accounting method to cash basis accounting, you will ordinarily need to request permission to do so by filing Form 3115 with the IRS.