What are the sections of the Urla?

Additional Questions by URLA Section

- Section 1 | This section identifies the borrower(s), where (s)he lives, how (s)he earns income and how much.

- Section 2 | Covers Assets and Liabilities.

- Section 3 | Deals with any real estate the borrower currently owns.

- Section 4 | About the loan and property.

What are the 10 sections of the Urla?

Terms in this set (10)

- Section I. Type of Mortgage and Terms of Loan; also contains a place to sign for the borrower and the co-borrower if they are applying for joint credit.

- Section II. Property Information & Purpose of Loan.

- Section III.

- Section IV.

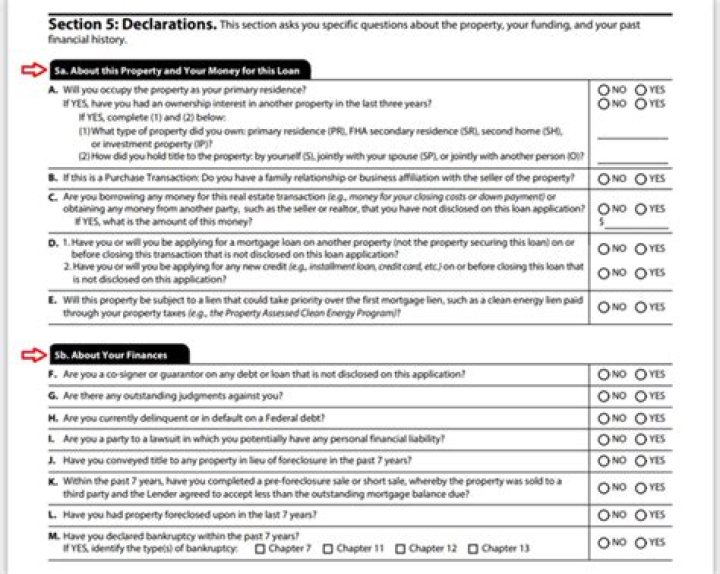

- Section V.

- Section VI.

- Section VII.

- Section VIII.

What field on the lender loan information page should a unit number be entered in?

may be different for FHA, VA, USDA-RD, and Conventional loans). If you are unsure, ask your Lender to clarify. If the street address includes a unit number, enter it in the “Unit #” field.

Which borrower information is contained in the Uniform Residential loan Application Urla )?

When filling out this application, you’ll be asked to supply an array of personal information, including your Social Security number, date of birth, marital status, address, monthly income, work history, assets and liabilities. Lenders in the U.S. have used the URLA for more than 20 years.

What is H in property status?

Hold (H): Hold is for properties that have been temporarily removed from the active status and are still listed with intention of returning to active status in a short period of time.

What new section replaces the detail of transaction on the 2020 Urla in the lender loan section?

Section L4

Section L4: The last page of the Lender Loan Information form focuses on Qualifying the Borrower. This will replace Details of Transaction on the current 1003.

Can unmarried borrowers be on the same 1003?

Answer: by Jim Bedsole: To be clear – if you require unmarried joint applicants to complete separate 1003 applications, but don’t require married joint applicants to complete separate 1003 applications, that is discrimination based on marital status, which violates both ECOA/Regulation B.

What is considered a complete 1003?

The 1003 loan application, or Uniform Residential Loan Application, is the standardized form used by most mortgage lenders in the U.S. for mortgages they purchase from lenders. The application asks questions about the borrower’s employment, income, assets, and debts, as well as requiring information about the property.

What is S PS R and H property status?

STATUS OF PROPERTY – For each property listed, show its current status; “S” if sold, “PS” if presently listed for sale, and “R” if the property is currently being rented or will be rented.

When do I need a tax ID number for a trust?

If an irrevocable trust earns more than $600 in income during the calendar year, the trustee will be required to file a 1041 tax return using the unique Federal Tax ID number. The Federal Tax ID number is also required to open a bank account under the trust name.

When does a trust have to file an income tax return?

As a result, these trusts will be required to file an annual T3 return even where one is not currently required. 1. Currently, when does a trust have to file an income tax return? Generally, a trust has to file an annual income tax (T3) return if the trust has tax payable or it distributes all or part of its income or capital to its beneficiaries.

Can a grantor of a trust get a new Social Security number?

While the grantor is still alive, the trust does not file a separate income tax return. After the grantor dies, his social security number must be replaced by a Federal Tax ID Number (TIN). The trustee can get a new TIN by using IRS Form SS-4. One of the reasons for this requirement is that while the grantor is alive, the trust is revocable.

How is the filing requirement changing for trusts?

2. How is the filing requirement changing for trusts? For 2021 and subsequent taxation years, Budget 2018 proposes that all non-resident trusts that currently have to file a T3 return and express trusts that are resident in Canada, with some exceptions, will have to provide additional information on an annual basis.