What are the three levels of variance analysis?

The three-way analysis shows the difference between the total actual factory overhead and total standard factory overhead costs split into three components: spending variance, efficiency variance, and volume variance.

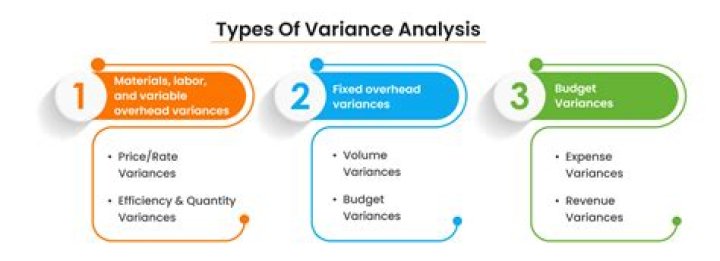

What are the three types of variance?

Variance means the deviation of actual from standard. In other words variance is the difference between the actual performance and standard performance….It may be grouped into three categories as under:

- Material Cost Variance (MCV),

- Labour Cost Variance (LCV),

- Overhead Cost Variance (OCV).

What is Level 3 variance?

Sales Volume Variance- It is a difference between flexible budget amounts and static budget amounts. Level- 3 Analysis- Basically it is cost variance analysis. Variances of direct cost are calculated in this level, Such as for direct material cost and for direct labour cost.

What is the four variance method?

4-Variance analysis is a method that classifies spending, efficiency and volume variances into the fixed and variable parts.

What is the formula for direct materials efficiency variance?

To calculate a direct materials efficiency variance, the formula is (actual quantity used × standard price) − (standard quantity allowed × standard price).

How do you explain revenue variance?

Revenue variance results from the differences between budgeted and actual selling prices, volumes or a combination of the two.

- Price. A favorable or unfavorable revenue variance occurs if the actual selling price is greater or less than the budgeted selling price, respectively.

- Volume.

- Profit.

- Budget.

What are different types of variance?

Types of variances

- Variable cost variances. Direct material variances. Direct labour variances. Variable production overhead variances.

- Fixed production overhead variances.

- Sales variances.

What is the cost variance?

Cost variance is the process of evaluating the financial performance of your project. This is calculated by finding the difference between BCWP (Budgeted Cost of Work Performed) and ACWP (Actual Cost of Work Performed).

How is cost variance calculated?

Cost Variance can be calculated using the following formulas:

- Cost Variance (CV) = Earned Value (EV) – Actual Cost (AC)

- Cost Variance (CV) = BCWP – ACWP.

How do you calculate activity variance?

It is calculated as the average squared deviation of each number from the mean of a data set. For example, for the numbers 1, 2, and 3 the mean is 2 and the variance is 0.667.

When to use three or four variance in overhead analysis?

Variance analysis for overhead normally focuses on efficiency variances for machinery and indirect production costs The efficiency variance computed on a three-variance approach is equal to the efficiency variance computed in the four-variance approach

How are spending variances calculated in a three way analysis?

The three-way analysis variances can be computed as follows: A more expanded breakdown known as “four-way analysis” simply separates the spending variance into the variable and fixed components. The four-way analysis consists of: 1.) variable spending variance, 2.) fixed spending variance, 3.) efficiency variance, and 4.) volume variance.

How is the efficiency variance of a unit calculated?

The efficiency variance is usually calculated separately for each of the following costs: Direct materials. This is called the material yield variance, and is calculated as: (Actual unit usage – Standard unit usage) x Standard cost per unit. Direct labor.

When is efficiency variance applied to direct labor?

The efficiency variance can be applied to direct labor. This is called the labor efficiency variance, and is technically related more to material usage than to efficiency. It is calculated as: The efficiency variance can be applied to overhead.