What can be taken off of taxes?

Here are some of the most common deductions that taxpayers itemize every year.

- Property Taxes.

- Mortgage Interest.

- State Taxes Paid.

- Real Estate Expenses.

- Charitable Contributions.

- Medical Expenses.

- Lifetime Learning Credit Education Credits.

- American Opportunity Tax Education Credit.

What are the new taxes for 2021?

The income taxes assessed in 2021 are no different. Income tax brackets, eligibility for certain tax deductions and credits, and the standard deduction will all adjust to reflect inflation. For most married couples filing jointly their standard deduction will rise to $25,100, up $300 from the prior year.

How are taxes taken out of your paycheck?

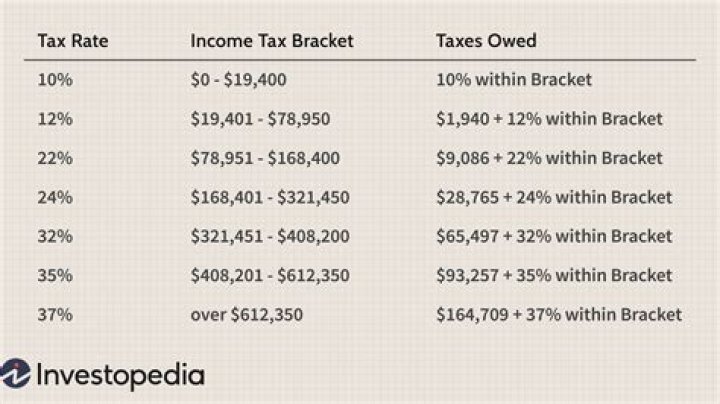

The amount of money you earn during your pay period, when viewed with your filing status, determines your income bracket and associated federal income tax rate. For 2021 tax brackets, visit this page from The Tax Foundation. Your taxes may also be impacted if you contribute a portion of your paycheck to a tax-advantaged retirement savings account.

What kind of deductions can I take on my taxes?

1. Standard Tax Deduction If you did the math and didn’t have enough itemized deductions to get you above $6,350 for singles and $12,700 for marrieds, you can take the standard tax deduction. If you are filing as head of household, you can deduct $9,350. 2. Reinvested Dividends Do you have a Betterment account?

How to tell if federal tax refund will be offset ( taken )?

You may not have anyone else call for you, nor may you call on anyone else’s behalf, this is a criminal offense – don’t do it. You will need to enter your Social Security number when prompted by the recording; this will search the database and let you know if there is an impending offset.

What to do if you make a mistake on your tax return?

On form 1040X, in Column A, you’ll briefly summarize the items on your tax return as originally reported. In Column B, you’ll indicate any adjustments for items of income, deductions, liabilities, and payments. In Column C, you’ll report the correct amounts as they should have appeared on the original tax return.