What closing entries are made?

A closing entry is a journal entry made at the end of the accounting period. It involves shifting data from temporary accounts on the income statement to permanent accounts on the balance sheet. All income statement balances are eventually transferred to retained earnings.

Do you close adjusting entries?

First, adjusting entries are recorded at the end of each month, while closing entries are recorded at the end of the fiscal year. And second, adjusting entries modify accounts to bring them into compliance with an accounting framework, while closing balances clear out temporary accounts entirely.

What is the one financial statement that can be presented after closing entries are made?

Statement of Retained Earnings

The closing entries are the journal entry form of the Statement of Retained Earnings. The goal is to make the posted balance of the retained earnings account match what we reported on the statement of retained earnings and start the next period with a zero balance for all temporary accounts.

Why are permanent accounts not closed?

The reason they are called permanent accounts is because they are never closed at the end of an accounting period. Temporary accounts include revenues, expenses, and withdrawals. They are closed at the end of every year so as not to be mixed with the income and expenses of the next periods.

What is the purpose of closing entries What accounts are not affected by closing entries?

The Purpose of Closing Entries Accountants perform closing entries to return the revenue, expense, and drawing temporary account balances to zero in preparation for the new accounting period.

Why nominal accounts are closed?

Nominal Accounts They’re also known as temporary accounts. Nominal accounts track transactions that affect your income statement, such as revenues, expenses, gains and losses, according to Accounting Tools. You close them out by transferring the balances.

What do closing entries do to an account?

Definition of Closing Entries. Closing entries transfer the balances from the temporary accounts to a permanent or real account at the end of the accounting year. As a result, the temporary accounts will begin the following accounting year with zero balances.

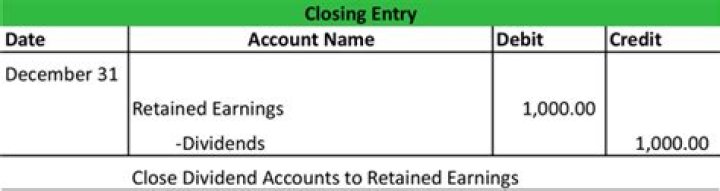

What are the closing entries on the statement of retained earnings?

The closing entries are the journal entry form of the Statement of Retained Earnings. The goal is to make the posted balance of the retained earnings account match what we reported on the statement of retained earnings and start the next period with a zero balance for all temporary accounts.

When do you close an income statement account?

The closing of the income statement accounts (revenues, expenses, gains, losses) by transferring their balances to the owner’s capital account or the corporation’s retained earnings account. This is done after the company’s financial statements for the year have been prepared.

When do you make a closing entry in a journal?

What is a Closing Entry? A closing entry is a journal entry that is made at the end of an accounting period to transfer balances from a temporary account to a permanent account.