What comes after the adjusted trial balance?

Debits and credits should always match in a trial balance. Remember not to confuse adjusting entries with closing entries. Closing entries are completed after the adjusted trial balance is completed.

What is the purpose of closing journal entries?

Understanding Closing Entries The purpose of the closing entry is to reset the temporary account balances to zero on the general ledger, the record-keeping system for a company’s financial data. Temporary accounts are used to record accounting activity during a specific period.

What does the adjusted trial balance show?

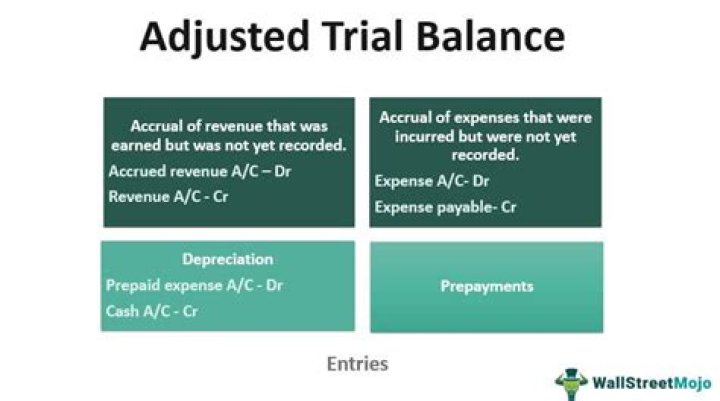

An adjusted trial balance shows the balances of all accounts, including those that have been adjusted, at the end of an accounting period. Its purpose is to prove the equality of the total debit balances and total credit balances in the ledger after all adjustments.

Does the adjusted trial balance list temporary accounts?

It is the third (and last) trial balance prepared in the accounting cycle. Since temporary accounts are already closed at this point, the post-closing trial balance will not include income, expense, and withdrawal accounts. It will only include balance sheet accounts, a.k.a. real or permanent accounts.

What happens if prepaid expenses are not adjusted?

What Happens if Prepaid Expenses Are Not Adjusted on a Financial Statement? If prepaid expenses are not adjusted, they will be overstated and the expenses actually incurred understated. A misrepresentation of prepaid expenses and incurred expenses will have an impact on both the balance sheet and the income statement.

How do you prepare closing entries from an adjusted trial balance?

Four Steps in Preparing Closing Entries

- Close all income accounts to Income Summary.

- Close all expense accounts to Income Summary.

- Close Income Summary to the appropriate capital account. Owner’s capital account for sole proprietorship.

- Close withdrawals/distributions to the appropriate capital account.