What do you need to know about 1031 exchange rules?

Everything you need to know about 1031 exchange rules by Brad Cartier, posted in Finances, Guides, Legal & Taxes Rental property finances made easy. Learn More Savvy real estate investors know that 1031 exchanges are commonly used to defer paying capital gains tax and/or completely eliminate them through estate planning.

How long can you rent a 1031 exchange property?

rent that property at fair market value (FMV) for 14 days or more and limit using §1031 exchange property for personal residence to under 15 days or 10% of days during the 12-month period that the property is rented at FMV. But of course, these rules aren’t mandated. That would require Congressional action.

How are funds held in escrow in a 1031 exchange?

It’s important to note that investors cannot receive proceeds from the sale of a property while a replacement property is being identified and purchased. Instead, funds are held in escrow by a 1031 exchange intermediary—sometimes referred to as an accommodator—until the replacement property is purchased.

What are safe harbor rules for exchange properties?

Revenue Procedure 2008-16 safe harbor rules are a de facto release precluding the IRS from interjecting any waiting time implications. It’s a head start in substantiating true intent. Turning over exchange properties just acquired immediately are problematic at best. For very quick turnovers a plausible defense is likely needed.

Can a 1031 exchange apply to a former primary residence?

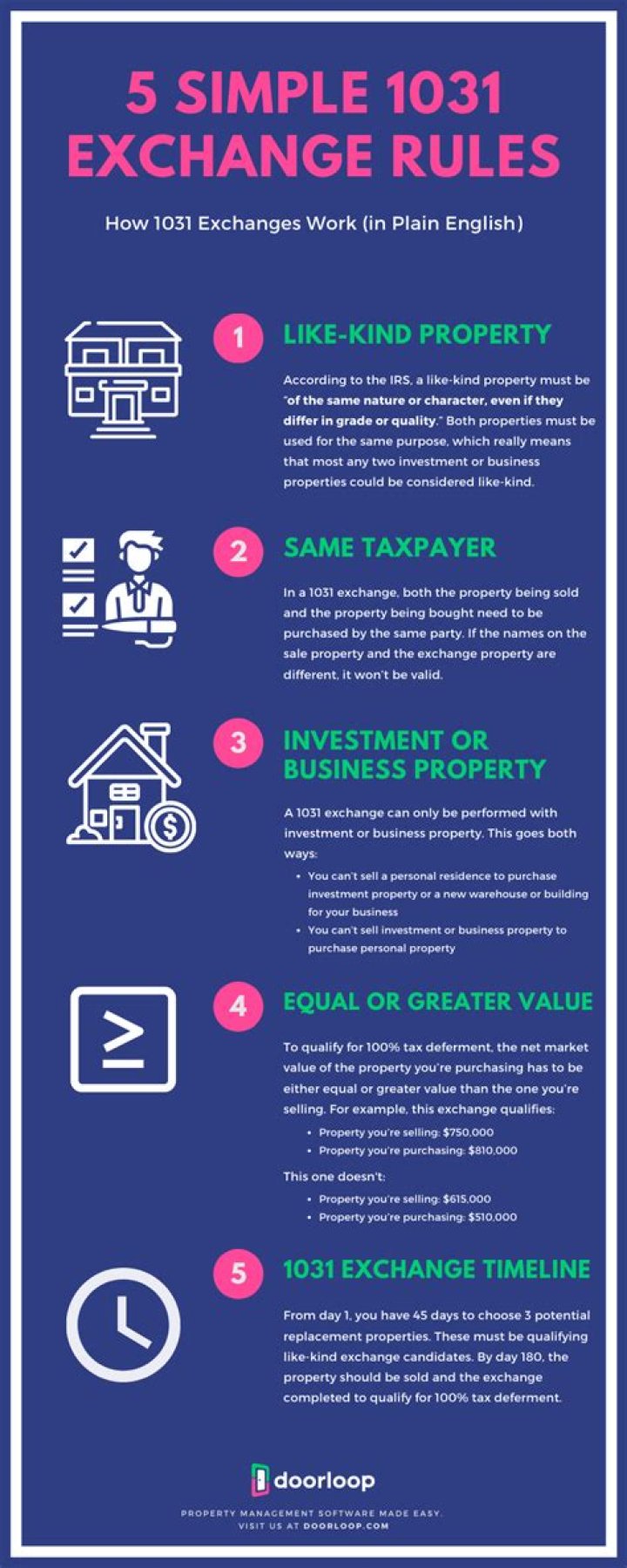

The 1031 provision is for investment and business property, although the rules can apply to a former primary residence under certain conditions.

How long does it take to get a new home on 1031 exchange?

The Replacement Property must be identified within 45 days. The Replacement Property must be received within 180 days (or the federal tax due date, including extension, if earlier). Principal Residences do not qualify.

Is there an exception to IRC Section 1031?

IRC Section 1031 provides an exception and allows you to postpone paying tax on the gain if you reinvest the proceeds in similar property as part of a qualifying like-kind exchange.