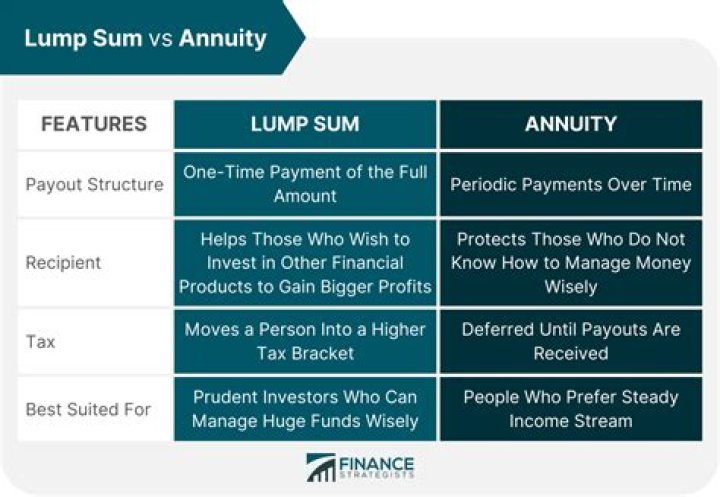

What does initial lump sum mean?

A lump-sum payment is an often large sum that is paid in one single payment instead of broken up into installments. They are sometimes associated with pension plans and other retirement vehicles, such as 401k accounts, where retirees accept a smaller upfront lump-sum payment rather than a larger sum paid out over time.

Do you have to pay taxes in one lump sum?

A lump sum amount can be rolled over to an Individual Retirement Account (IRA) and avoid taxation when you receive the lump sum. If the money isn’t rolled over, you’ll pay ordinary income tax on the amount of the lump sum.

Is lump sum E included in gross?

Most commonly you would have a Lump Sum E when you make a back payment of salary and wages relating to a period of time more than 12 months before the date that the back pay itself is being paid. If it is not, it will just go in the gross income box of the payment summary.

How are lump sum payments taxed in Canada?

Certain qualifying retroactive lump-sum payments are eligible for a special tax calculation. For all other lump-sum payments, deduct income tax using the withholding rates for lump-sum payments. Report certain lump-sum payments on a T4A, Statement of Pension, Retirement, Annuity, and Other Income.

How are lump sum payments treated as pay?

This is then multiplied by the number of year’s service. Any tax free lump sum payments you receive are then taken from this benefit. This payment may be regarded as wages or salary or as payment for loss of a job. If your contract provides for payment in lieu of notice, the payment is treated as pay and exemptions do not apply.

How does the US tax UK pension lump sum payments to US?

In summary, a UK 25% lump-sum pension distribution is fully taxable to a US citizen and resident and the US tax authorities have specifically stated that the Treaty language agrees. Any other position on this issue contradicts the IRS’s position and, quite frankly, has no basis either in US tax law or the Treaty itself.

How to defer tax on a lump sum payment?

You may be able to defer tax on all or part of a lump-sum distribution by requesting the payer to directly roll over the taxable portion into an individual retirement arrangement (IRA) or to an eligible retirement plan.