What does physical presence mean for taxes?

In international taxation, a physical presence test is a rule used to determine tax residence of a natural or legal person. It may rely on having a place of business in the jurisdiction (for legal persons), or remaining in or out of the jurisdiction for a certain number of days each year (for natural persons).

What does physical presence mean?

Physical presence refers to the number of days the applicant must physically be present in the United States during the statutory period up to the date of filing for naturalization. The continuous residence and physical presence requirements are interrelated but each must be satisfied for naturalization.

How does the physical presence test work for the IRS?

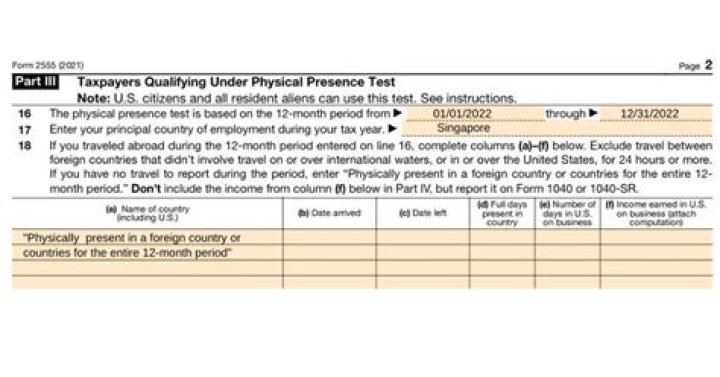

What Is the Physical Presence Test? The physical presence test is a tool used by the Internal Revenue Service (IRS) to determine whether a taxpayer qualifies for the foreign earned income exclusion when filing their taxes. The test requires that a person be physically present in a foreign country or countries for at least 330 full days …

What do you need to know about the physical presence test?

The physical presence test is a tool used by the Internal Revenue Service (IRS) to determine whether a taxpayer qualifies for the foreign earned income exclusion when filing their taxes. The test requires that a person be physically present in a foreign country or countries for at least 330 full days during a consecutive 12 months.

How long do you have to be in a foreign country to pass the physical presence test?

330 Full Days. Generally, to meet the physical presence test, you must be physically present in a foreign country or countries for at least 330 full days during the 12-month period. You can count days you spent abroad for any reason. You do not have to be in a foreign country only for employment purposes.

Do you have to be a bona fide resident to get the physical presence test?

Income earned abroad may qualify for the foreign earned income exclusion, the foreign housing exclusion or deduction, as long as the income is earned in the taxpayer’s tax home and the taxpayer meets either the bona fide resident test or the physical presence test.