What happens to a revocable living trust when the grantor dies?

Trust Administration After Grantor’s Death For an individual revocable trust, the death of the grantor is generally a triggering event. After it occurs, the successor trustee, usually appointed in the trust agreement, administers and distributes the assets as specified in the governing document.

Does a living trust require a tax return?

No separate tax return will be necessary for a Revocable Living Trust. However, even though the Grantor is taxed on the Trust income, the assets are legally held by the Trust, which will survive the Grantor’s death. That is why the assets in the Trust do not need to go through the probate process.

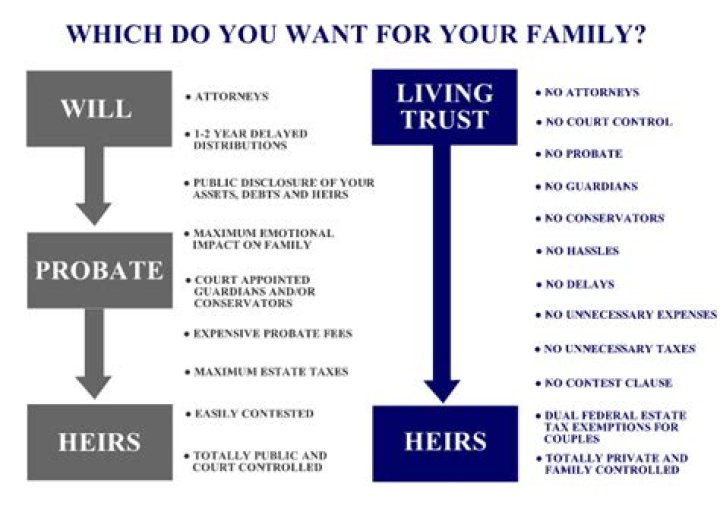

A revocable living trust is a legal entity that holds a trustmaker’s property so probate of that property isn’t necessary when the trustmaker—sometimes called the grantor—dies. A deceased individual can’t own property, so probate becomes necessary to move assets from the decedent’s ownership into the names of living beneficiaries upon death.

What do you call a trust when your mother dies?

You pick entity: trust; next screen: irrevocable trust (because that’s what the trust became when your mother died). Then you continue on with your information as…

Who is the principal of a revocable trust?

The money or property held by the trustee for the benefit of someone else is the principal of the trust. The principal changes often due to the trustee’s expenses or the investment’s appreciation or depreciation. The collective assets comprise the trust fund. The person or people benefiting from the trust are the beneficiaries.

Are there any tax advantages to a revocable trust?

Costs of maintaining a revocable trust are greater than other estate planning tools such as a will. A revocable trust does not offer the grantor tax advantages. Since not all assets will be included in the revocable trust, the grantor must create a will to designate beneficiaries for the remaining assets,…

How do you know if a trust is revocable or irrevocable?

Usually, if trusts are created on the death of the settlor (your grandmother) for each of her children for the child’s lifetime, the trusts are irrevocable.

Are there any trusts in California that are irrevocable?

In general, all trusts set up in California are revocable unless they state that they are irrevocable in the trust document itself. As your grandmother died, likely having a revocable trust while she was alive, it is likely that the trusts for your father and your aunt are irrevocable trusts.

How much does the FDIC cover a revocable living trust?

The FDIC (Federal Deposit Insurance Corporation) typically protects money in a bank account up to $250,000. However, that coverage amount goes up with revocable living trusts. According to the FDIC, the owner of a revocable trust account receives insurance of up to $250,000 per each beneficiary.

What do you do with a living trust?

A living trust is a form of estate planning set up by a person during their lifetime that allows them to continue benefiting from their assets while they are living and helps manage the distribution of their property when they pass away.

What to do when the owner of a trust dies?

You have an ongoing duty to provide information to the owner’s beneficiaries when the settlor dies. You should consult the laws of your jurisdiction and an estate attorney to find out what information you must provide. You will also likely need to provide ongoing information to the beneficiaries regarding the status of the account.

What happens to an estate when the owner passes away?

When the owner passes away, the successor trustee must begin managing the estate and distributing assets in accordance with the terms of the planning document. The owner, called the settlor, is the person who sets up the estate account while they are alive.