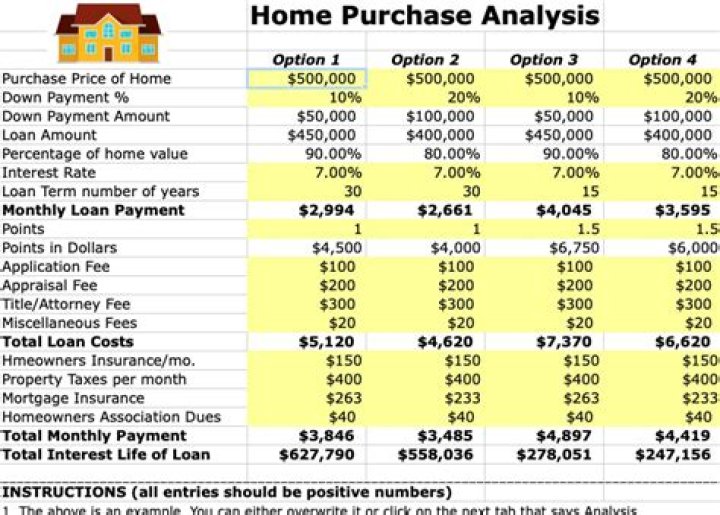

What house purchase costs are tax deductible?

3. Are mortgage closing costs tax deductible? In general, the only settlement or closing costs you can deduct are home mortgage interest and certain real estate taxes. You deduct them in the year you buy your home if you itemize your deductions.

How do you write off buying a house?

- Mortgage interest. For most people, the biggest tax break from owning a home comes from deducting mortgage interest.

- Points.

- Real estate taxes.

- Mortgage Insurance Premiums.

- Penalty-free IRA payouts for first-time buyers.

- Home improvements.

- Energy credits.

- Tax-free profit on sale.

When do you get a tax deduction for buying a home?

The way it works is if you bought your home before December 15th, 2017 you’re entitled to deduct interest payments up to $1 million in loans that you used for buying a home, building a home, home improvement, or purchasing a second home. However, if you made the purchase after this date there are changes.

Do you get a mortgage interest deduction when you sell your home?

As with property taxes, you can deduct the interest on your mortgage for the portion of the year you owned your home.

What can you not deduct on your taxes when you own a home?

What can’t I deduct? You can’t deduct the following payments for a personal residence: Dues to a homeowners association; Insurance on your home; Appraisal fees for your home; The cost of improvements to your home, except in the relatively rare case where they qualify as a medical expense. (But keep those receipts.

What are the tax deductions for a home equity line of credit?

The interest on up to $100,000 borrowed on a home equity loan or home equity line of credit, regardless of the reason for the loan (for tax years prior to 2018 only). Points that you paid when you purchased the house (or those that you convinced the seller to pay for you). Home improvements required for medical care.