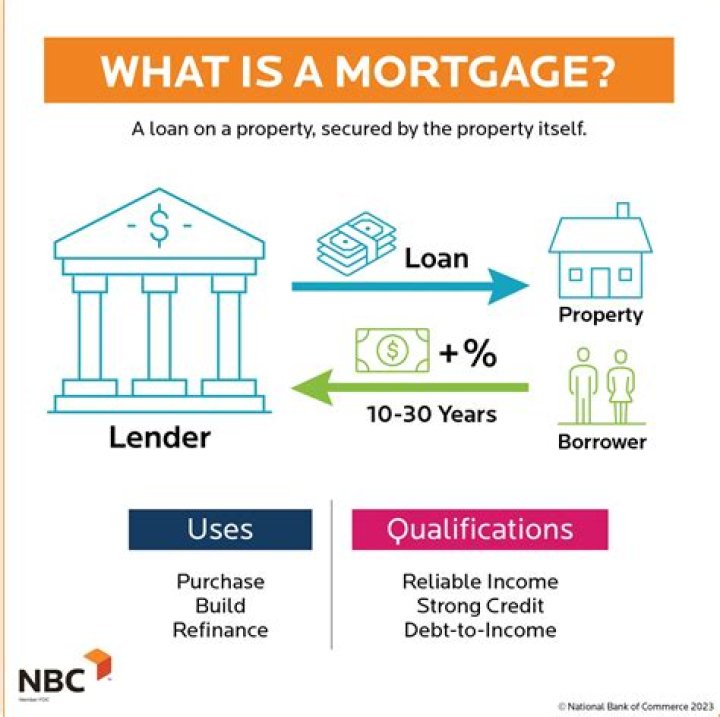

What is a forgiven mortgage loan?

Mortgage forgiveness means exactly what the term suggests: The lender actually forgives some or all of the debt you owe. That is, it simply wipes away that portion of your debt. After all, it extended the mortgage — a loan of money guaranteed by your house — in anticipation of being paid back at some point.

Do banks forgiven mortgage debt?

There is no mortgage forgiveness. Far more common and beneficial to the borrower is a nonjudicial foreclosure. In a nonjudicial foreclosure, the lender follows a specific set of foreclosure rules and procedures established by the state.

Do banks forgive debt?

Debt forgiveness is simple in theory: a lender forgives some or all of the debt you still owe on a loan. But this undeniably appealing concept almost always comes with strings attached. Before seriously considering debt forgiveness as an option, keep your eyes open and avoid the pitfalls of wishful thinking.

Can you get your mortgage forgiven if you sell your second home?

Let’s say you owe $200,000 on your first mortgage and $50,000 on your second. Your first lender forecloses on the home and sells it for $190,000. He may feel satisfied to keep the $190,000 and forgive the $10,000 outstanding debt since he recovered most of his loss.

What are the rules for mortgage debt forgiveness?

Under the act, taxpayers were able to exclude up to $2 million in debt forgiveness, whether through foreclosure, short sale, or some sort of mortgage modification. The key stipulation: The waiver had to be made on the taxpayer’s qualified principal residence. Second homes and vacation homes did not qualify. All good, right?

What’s the best way to get debt forgiveness?

Short Sale. One way to seek debt forgiveness from your lender is to request a short sale. In a short sale, your lender agrees to accept the sale price of your home as payment of your mortgage in full, even if the house sells for less than what you owe.

What happens if I don’t pay my second mortgage?

After chapter 7 bankruptcy, I often advise my clients, just don’t pay the second mortgage. Now, if you don’t file bankruptcy and stop paying the second mortgage, two things would happen. They will call you day and night; and eventually they would sue you and garnish you.