What is considered qualified small business stock?

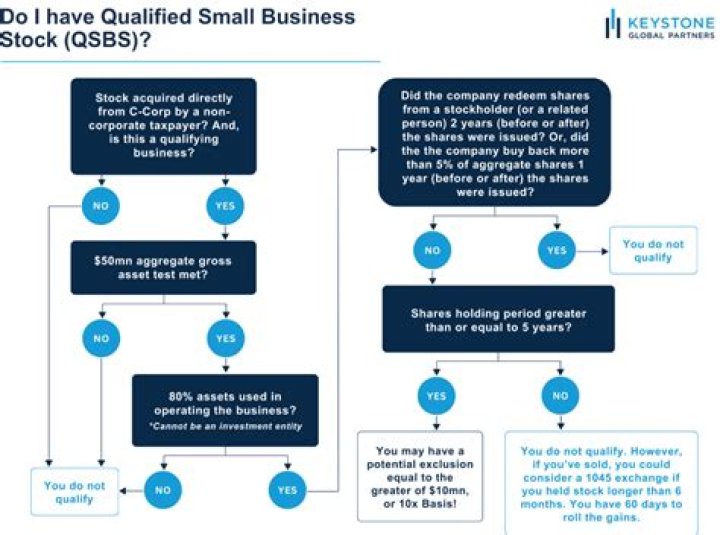

A qualified small business stock (QSBS) is any stock acquired from a QSB after Aug. 10, 1993. The investor must have held the stock for at least five years. At least 80% of the issuing corporation’s assets must be used in the operations of one or more of its qualified trades or businesses.

What is a 1045 rollover?

Qualified Rollovers (Section 1045) The tax code allows taxpayers to sell QSBS and to defer capital gain on the sale if they roll the sales proceeds into replacement QSBS within 60 days of the sale. The taxpayer must reinvest the entire sales proceeds (not just gain) in replacement QSBS within 60 days of the sale.

Do stock options qualify for Qsbs?

Stock Options can qualify for the QSBS tax exemption, pursuant to IRC Section 1202, if certain conditions are met, included but not limited to ensuring that the underlying company meets the QSBS criteria at the time the options are exercised and if the securities are held 5-years after exercise.

A qualified small business stock (QSBS) is any stock acquired from a QSB after Aug. 10, 1993. Under Section 1202, the capital gains from qualified small businesses are exempt from federal taxes.

When to roll over qualified small business stock?

For questions regarding the QSBS regime or the qualified rollover rules, please contact a member of the Tax Services Group. The tax code allows taxpayers to sell QSBS and to defer capital gain on the sale if they roll the sales proceeds into replacement QSBS within 60 days of the sale.

What are the benefits of a qualified rollover?

Taxpayers also can combine the benefits of a qualified rollover under section 1045 with gain exclusion under section 1202.

What are the requirements for a QSB rollover?

Here are some of the main requirements: The taxpayer must be an individual, trust, estate, or one of certain pass-through entities, but it cannot be a corporation. The taxpayer must acquire the QSBS from the issuer in an original issuance.

How are qualified small business stock ( qsbs ) treated?

Tax treatment for a QSB stock depends on when the stock was acquired and the length of its holding. The Protecting Americans from Tax Hikes Act (PATH Act), allows investors to exclude 100% of capital gains on qualified small business stock (QSBS) if the stock qualifies under Section 1202 of the IRC.