What is equity accounting?

The equity meaning in accounting refers to a company’s book value, which is the difference between liabilities and assets on the balance sheet. This is also called the owner’s equity, as it’s the value that an owner of a business has left over after liabilities are deducted.

What is goodwill associated with an equity method investment?

What is goodwill associated with an equity method investment? The excess of the cost of the investment that cannot be attributed to a specific investee asset or liability. When an investor purchases an investment for an amount excess of the investees book value, how is the excess amount allocated?

What is equity method vs cost method?

In general, the cost method is used when the investment doesn’t result in a significant amount of control or influence in the company that’s being invested in, while the equity method is used in larger, more-influential investments.

What is equity method of accounting for joint venture?

The equity method of accounting is used to assess the profits earned by their investments in other companies. This equity method of accounting is more commonly used when one company in a joint venture has a recognizably greater level of influence or control over the venture than the other.

Do you recognize goodwill under equity method?

Any excess cost that is not allocated to the identifiable net assets is considered equity method goodwill. In addition, no amount of the excess of the cost of the equity method investment over the investor’s share of the underlying net assets of the investee would be considered equity method goodwill.

Where do equity method investments appear on the balance sheet?

An equity method investment is recorded as a single amount in the asset section of the balance sheet of the investor. The investor also records its portion of the earnings/losses of the investee in a single amount on the income statement.

Is there goodwill in equity method?

Any excess cost that is not allocated to the identifiable net assets is considered equity method goodwill. The investor is also required to identify the deferred tax consequences of the equity method basis differences.

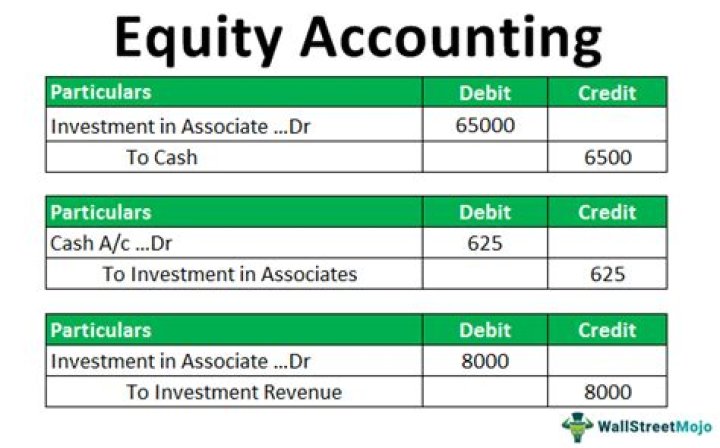

How do you account for equity method investments?

Equity method investments are recorded as assets on the balance sheet at their initial cost and adjusted each reporting period by the investor through the income statement and/or other comprehensive income ( OCI ) in the equity section of the balance sheet.

What are the two types of equity found on the balance sheet?

Investors should be aware that stockholders’ equity can decline as well as increase.

- Paid-in Capital. One of the two main sources of stockholders’ equity is paid-in capital.

- Retained Earnings. Retained earnings are the other main source of stockholders’ equity.

- Other Sources.

- Warning: Stockholders’ Equity Can Drop.

Does goodwill reduce equity?

Direct Impact of Goodwill on Stockholder’s Equity Since goodwill is not an asset that is created from income activities, it does not become part of retained earnings. As a result, it cannot be distributed among stockholders. Goodwill does not directly affect stockholder equity.

How do you calculate goodwill equity?

The goodwill calculation method is represented as, Goodwill Formula = Consideration paid + Fair value of non-controlling interests + Fair value of equity previous interests – Fair value of net assets recognized.