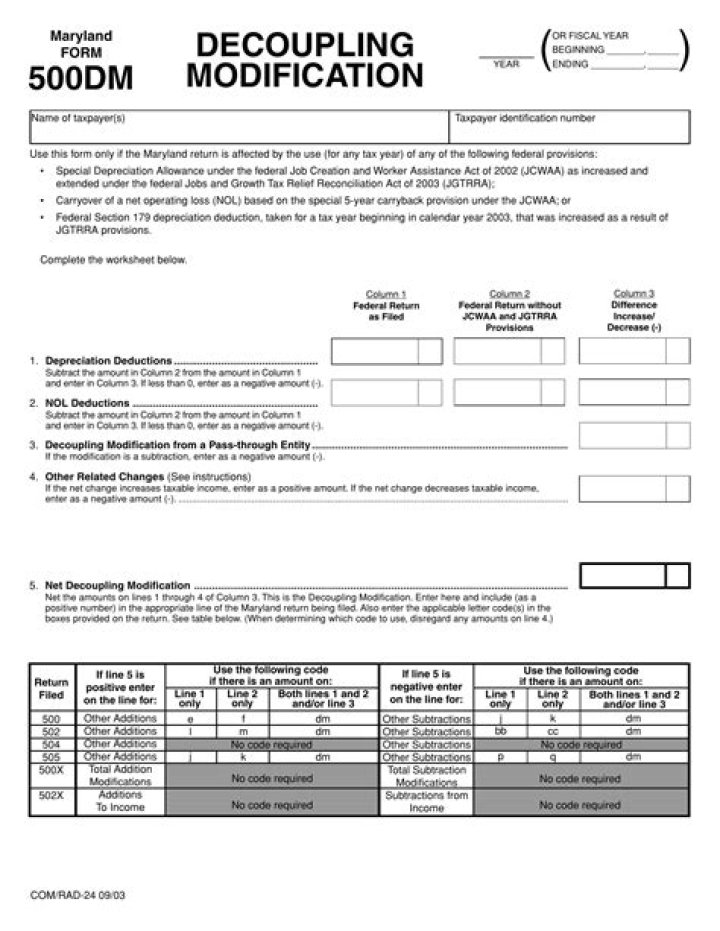

What is form 500DM?

Maryland has decoupled from certain federal provisions, as listed at the top of Form 500DM, by enacting addition and subtraction modifications which eliminate the effect of the changes on Maryland and local taxes. This form is used to determine the amount of the required modification.

Where to send Maryland form 502?

If you are sending a Form 502 or Form 505 (with a payment) through the US Postal Service, send it to: Comptroller of Maryland, Payment Processing, PO Box 8888, Annapolis, MD 21401-8888.

Does Maryland decoupling from bonus depreciation?

Maryland is already decoupled from bonus deprecation and enhanced Section 179 deductions, so there was no uncertainty there. Further, if depreciation from QIP creates a Maryland NOL in 2018 or 2019, that loss can be carried back, since it does not affect the 2020 tax year directly.

What is form 502 for?

Publication 502 explains the itemized deduction for medical and dental expenses that you claim on Schedule A (Form 1040), including: How to report the deduction on your tax return and what to do if you sell medical property or receive damages for a personal injury.

What is MD decoupling modification?

Does Maryland allow Section 179 deduction?

For Maryland tax purposes, a taxpayer only is allowed to expense up to $25,000, reduced dollar-for-dollar by the amount over $200,000, of the cost of Section 179 property that is purchased and put in service for a trade or business for the tax year.

Does Maryland follow the cares act?

The CARES Act became law on March 27, 2020. Therefore, Maryland is automatically decoupled from the CARES Act provisions affecting tax year 2020, but conforms to CARES Act provisions affecting tax years 2018 and 2019. The Maryland impact of each key provision is discussed below.

Does Maryland allow NOL carryback?

NOL Carryover Provisions Maryland allows net operating loss (NOL) deduction under I.R.C. § 172 to carryback for up to two years, without regard to any special federal provision allowing an election under I.R.C. § 172(b)(1)(H) to carryback the NOL for up to 5 years.