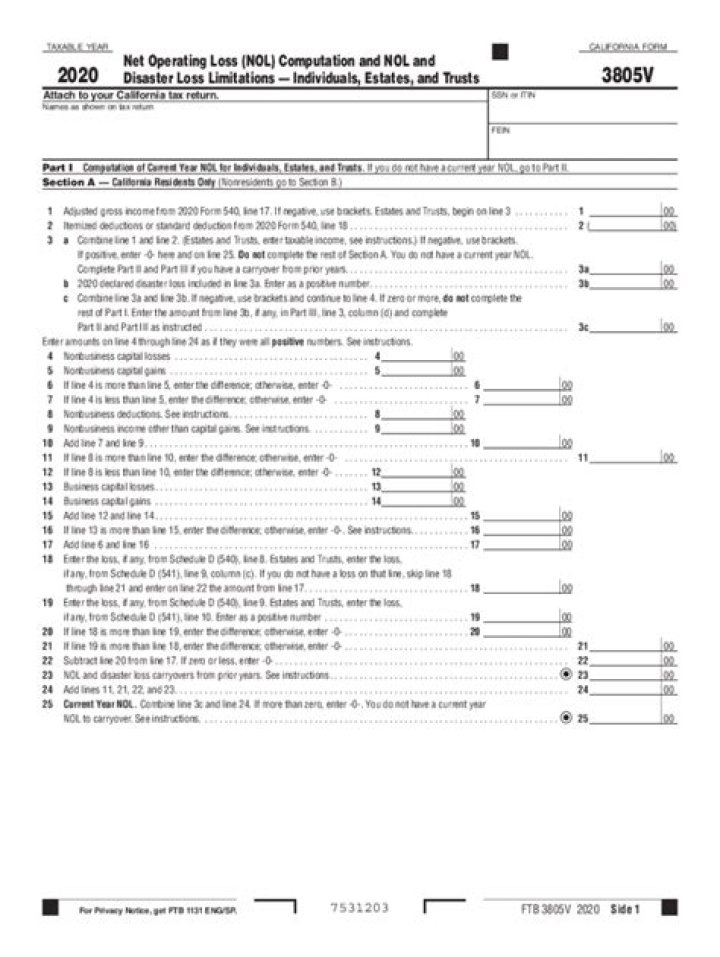

What is FTB Form 3805V CA?

Individuals, estates, or trusts use form FTB 3805V, to figure the current year NOL and to limit the NOL carryback/carryover and disaster loss deductions. Corporations use form FTB 3805Q, Net Operating Loss (NOL) Computation and NOL and Disaster Loss Limitations — Corporations.

Can you carry back CA NOL?

Overview. If your deductions and losses are greater than your income from all sources in a tax year, you may have a net operating loss (NOL). You may be able to claim your loss as an NOL deduction. This deduction can be carried back to the past 2 years and/or you can carry it forward to future tax years.

Can an individual carryback a net operating loss?

For individuals, an NOL may also be attributable to casualty losses. NOLs arising in tax years beginning in 2018, 2019, and 2020 may be carried back for a period of five years and carried forward indefinitely. A taxpayer may elect to forego the carryback.

Can California R&D credit offset AMT?

Other Provisions and Limitations of the RDC. However, the credit may not be used in these years to offset the corporate Minimum Tax, the Alternative Minimum Tax (AMT) under the PIT and the CT, or certain other taxes levied on Subchapter S corporations (such as taxes on built-in gains and excess net passive income).

What do I need to know about FTB 3805v?

Individuals, estates, or trusts use form FTB 3805V, Net Operating Loss (NOL) Computation and NOL and Disaster Loss Limitations – Individuals, Estates, and Trusts, to figure the current year NOL and to limit the NOL carryover and disaster loss deductions.

What are the instructions for the California tax form?

The instructions provided with California tax forms are a summary of California tax law and are only intended to aid taxpayers in preparing their state income tax returns. We include information that is most useful to the greatest number of taxpayers in the limited space available.

When does California conform to the Internal Revenue Code?

In general, for taxable years beginning on or after January 1, 2015, California law conforms to the Internal Revenue Code (IRC) as of January 1, 2015. However, there are continuing differences between California and federal law. When California conforms to federal tax law changes, we do not always adopt all of the changes made at the federal level.

When did the TTA and Mea tax incentives expire?

The Targeted Tax Areas (TTA) and Manufacturing Enhancement Areas (MEA) both expired on December 31, 2012. For more information, go to ftb.ca.gov and search for repeal tax incentives. Generally, no further EZ incentives can be generated after the expiration or repeal date.