What is imputed income for domestic partners?

The imputed income is the cost of coverage for the employee’s domestic partner and/or partner’s children. That portion is considered imputed income by the IRS. Imputed income is in addition to your monthly plan cost.

How do you report domestic partner imputed income?

- The employee will have imputed income reported on Form W-2 equal to the FMV of the domestic partner’s (or child’s) coverage.

- This amount will also be subject to income tax withholding and employment taxes.

How do you account for imputed income?

Record imputed income on Form W-2 in Box 12 using Code C. Also, include the amount for imputed income in Boxes 1, 3, and 5. Remember that imputed income is typically not subject to federal income tax withholding. However, imputed income is subject to Social Security tax and Medicare tax withholding.

Is imputed income considered earned income?

Unless specifically exempt, imputed income is added to the employee’s gross (taxable) income. But it is treated as income so employers need to include it in the employee’s form W-2 for tax purposes. Imputed income is subject to Social Security and Medicare tax but typically not federal income tax.

How does imputed income work for domestic partner?

If an employer pays for the domestic partner’s (or child’s) health coverage, then the FMV of the health coverage must be included in the employee’s income. The employee will have imputed income reported on Form W-2 equal to the FMV of the domestic partner’s (or child’s) coverage.

What does imputed income mean on health insurance?

When you offer family coverage that includes a domestic partner and that domestic partner’s child, the part of the premium that exceeds the employee portion is imputed income. This applies to any family-priced package you may offer. Imputed income also includes any individual policies that cover domestic partners and their children.

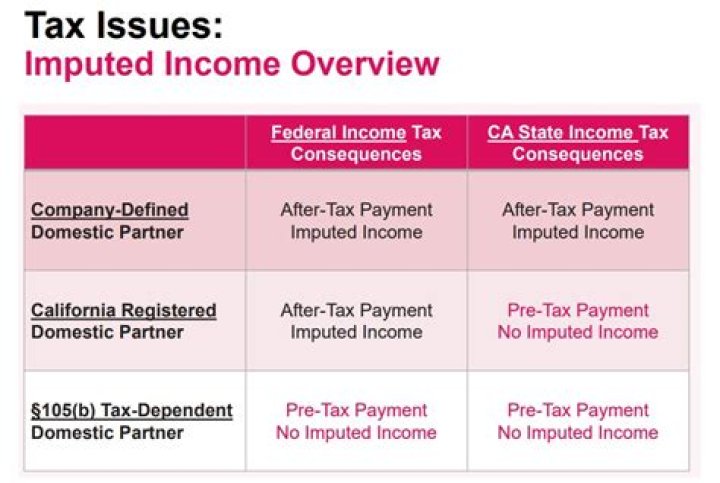

When does a domestic partner receive tax benefits?

Taxable Domestic Partner Benefits When health coverage is provided to a domestic partner (or to his or her child) who is not the employee’s Code §105(b) tax dependent depends on how coverage is paid for (pre-tax or after tax).

When is health coverage provided to a domestic partner?

When health coverage is provided to a domestic partner (or to his or her child) who is not the employee’s Code §105 (b) tax dependent depends on how coverage is paid for (pre-tax or after tax).