What is included in Inventoriable cost?

Inventoriable costs, also known as product costs, refer to the direct costs associated with the manufacturing of products and in getting them ready for sale. Often, inventoriable costs include direct labor, direct materials, factory overhead, and freight-in.

Which of the following can be classified as Inventoriable costs?

For a manufacturer, these costs include direct materials, direct labor, freight in, and manufacturing overhead. For a retailer, inventoriable costs are purchase costs, freight in, and any other costs required to bring them to the location and condition needed for their eventual sale.

Why are product cost sometimes called Inventoriable cost?

Product costs are often treated as inventory and are referred to as inventoriable costs because these costs are used to value the inventory. When products are sold, the product costs become part of costs of goods sold as shown in the income statement.

Are not Inventoriable costs?

Non-inventoriable cost: costs that are not included in the value of inventory, also known as non-manufacturing overhead. It includes Selling, General and Administrative expenses, and Interest expense. Name each of the basic inventory-related stock and flow accounts and explain their relationship to one another.

What is an example of manufacturing overhead?

Examples of Manufacturing Overhead depreciation, rent and property taxes on the manufacturing facilities. depreciation on the manufacturing equipment. repairs and maintenance employees in the manufacturing facilities. electricity and gas used in the manufacturing facilities.

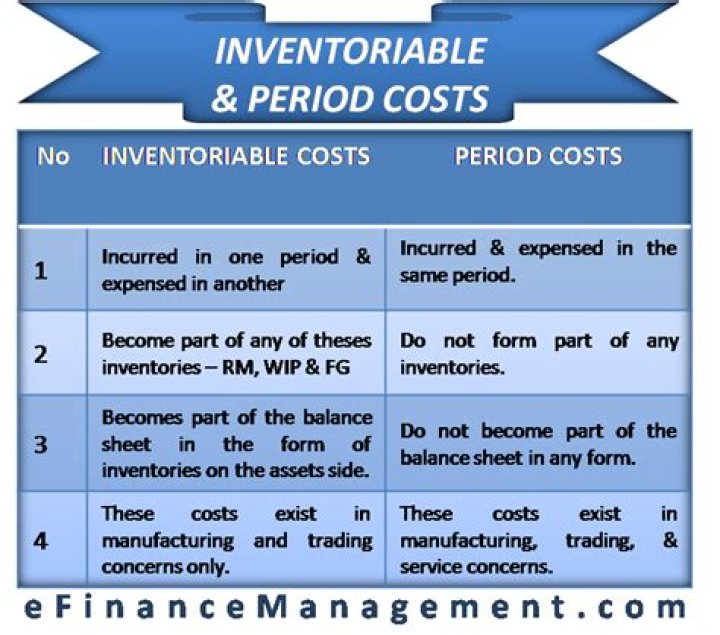

What are Inventoriable costs period costs?

Inventoriable costs can be defined as costs which become part of inventories such as raw material, work in progress and finished goods inventory present in the balance sheet of any business. Period costs are those costs which are incurred and expensed in Profit and Loss Statement in the period they are incurred.

Is the level of capacity utilization that managers?

It is the level of capacity utilization that managers expect for the current budget period, which is typically one year. It is the level of capacity that reduces theoretical capacity by considering unavoidable operating interruptions, such as scheduled maintenance time and shutdowns for holidays.