What is included on a traditional income statement?

A traditional income statement uses absorption or full costing, where both variable and fixed manufacturing costs are included when calculating the cost of goods sold. Companies are generally required to present traditional income statements for external reporting purposes.

For what purposes is the traditional income statement used?

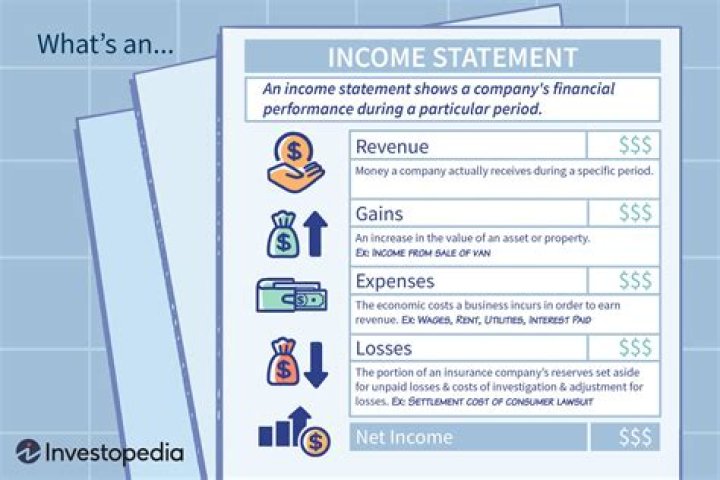

Also known as a profit and loss statement, a traditional income statement shows the extent to which a company is profitable or not during a given accounting period. It provides a summary of how the company generates revenues and incurs expenses through both operating and non-operating activities.

How do you calculate traditional income statement?

In a traditional income statement, cost of goods sold (variable + fixed) is subtracted from sales revenue to obtain gross profit figure and marketing and administrative expenses (variable + fixed) are then subtracted from gross profit figure to obtain net operating income.

What is the balance sheet also known as?

Overview: The balance sheet – also called the Statement of Financial Position – serves as a snapshot, providing the most comprehensive picture of an organization’s financial situation. It reports on an organization’s assets (what is owned) and liabilities (what is owed).

Is the traditional and common form of income statement?

A traditional income statement employs absorption costing to arrive at a profit or loss figure. This statement contains several blocks of revenue and expense information, which are organized as follows: This includes all expenses associated with the selling, general, and administrative functions of a business.

What is a CVP income statement?

A CVP or cost-volume-profit income statement has the same information as a more traditional income statement, but is designed to show the effects of changes in costs and volume on the profit of a business.

A traditional income statement shows the gross profit, operating profit and pretax and after-tax net income for an accounting period. Generally accepted accounting principles require companies to use the traditional income statement format for external reporting.

Do accountants prepare income statements?

Information from your accounting journal and your general ledger is used in the preparation of your business’s financial statement. The income statement, the statement of retained earnings, the balance sheet, and the statement of cash flows all make up your financial statements.

How do you do an income statement in accounting?

To write an income statement and report the profits your small business is generating, follow these accounting steps:

- Pick a Reporting Period.

- Generate a Trial Balance Report.

- Calculate Your Revenue.

- Determine Cost of Goods Sold.

- Calculate the Gross Margin.

- Include Operating Expenses.

- Calculate Your Income.

What does a traditional income statement look like?

How long does an income statement usually last?

Income Statement Accounting Period. An income statement usually covers a full year. That is most certainly the case when the income statement is prepared as part of a company’s published annual financial statements. However, the income statement may be drawn up for shorter periods, such as one month or three months (quarterly income statement).

When to use quarterly or annual income statement?

That is most certainly the case when the income statement is prepared as part of a company’s published annual financial statements. However, the income statement may be drawn up for shorter periods, such as one month or three months (quarterly income statement).

What’s the difference between traditional and contribution margin income statements?

Traditional and contribution margin income statements provide a detailed picture of a company’s finances for a given period of time. While both serve the purpose of showing whether a company has a net profit or loss, they differ in the way they arrive at that figure.