What is material participation in an S Corp?

Material participation is defined as when a taxpayer’s involvement in the business or trade is substantial, and it’s regular and continuous. Any work someone performs in an activity related to an interest they own is typically classified as participation, but it is not automatically material.

Is S Corp income active or passive?

If an S corporation has income earnings for the year, no more than 25 percent of its gross receipts for the year may be generated by passive income.

What is material income producing factor?

The capital is a material income-producing factor. This means that most of the money made by the business is due to the investment of this capital. Meaning income of the business consists principally of fees, commissions, or other compensation for personal services performed by members or employees of the partnership.

What is passive income S Corp?

Passive income is money your company didn’t earn from business activities such as manufacturing or providing services. Investment income such as dividends or interest is passive, for instance. If your S corporation owns rental real estate, the rental income is passive, unless the company actively manages the property.

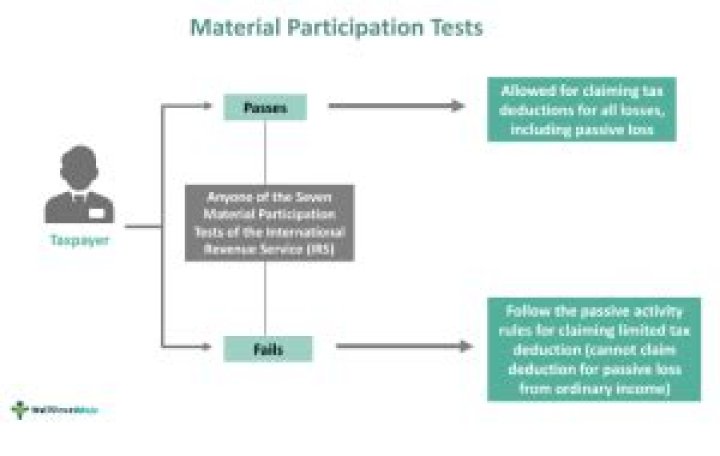

How is material participation determined on a individual basis?

Material participation is determined on an individual basis, and it’s determined each tax year. The opposite of material participation is called passive activity. If you haven’t materially participated in the business during the year, your share of any business deductions for the year is limited.

Who is a material participant in an S corporation?

A shareholder materially participates in an S corporation if the shareholder or the shareholder’s spouse is involved in the corporation’s trade or business on a regular, continuous, and substantial basis (Secs.

How many hours is material participation in a business?

The activity is a significant participation activity (SPA), and the sum of SPAs in which the taxpayer works 100 to 500 hours is more than 500 hours for the year. The taxpayer materially participated in the activity in any five of the previous 10 years.

Who is not a material participant in a partnership?

A limited partner of a partnership is not considered a material participant in activities of the partnership unless he or she meets Test 1 (the 500-hour test), Test 5 (the 5-out-of-10-year test), or Test 6 (the personal service activities test).