What is ordinary income in a partnership?

Business income from a partnership is generally computed in the same manner as income for an individual. That is, taxable income is determined by subtracting allowable deductions from gross income. This net income is passed through as ordinary income to the partner on Schedule K-1.

What is active or ordinary income?

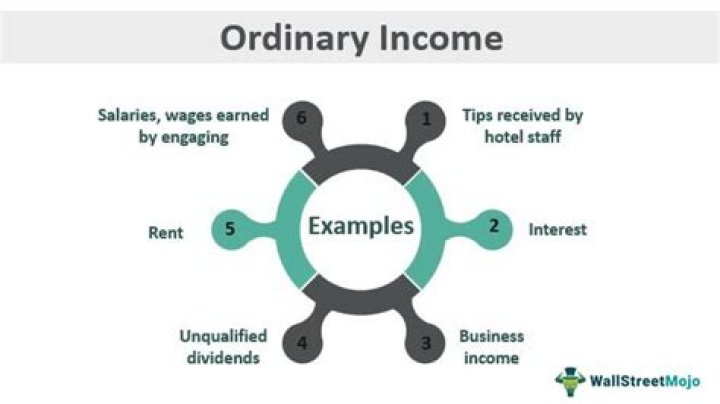

Active income refers to income received for performing a service. Wages, tips, salaries, commissions, and income from businesses in which there is material participation are examples of active income.

Is partnership income taxed ordinary income?

Reporting Partnership Income A partnership must file an annual information return to report the income, deductions, gains, losses, etc., from its operations, but it does not pay income tax. Instead, it “passes through” profits or losses to its partners.

Are partnership distributions ordinary income?

Unlike a regular corporation, a partnership isn’t subject to income tax. Rather, each partner is taxed on the partnership’s earnings, whether or not they are distributed. Similarly, if a partnership has a loss, the loss is passed through to the partners.

When does a partnership result in ordinary income or loss?

If a partner receives money or property in exchange for any part of a partnership interest, the amount due to his or her share of the partnership’s unrealized receivables or inventory items results in ordinary income or loss.

How are guaranteed payments treated on a partnership tax return?

For other tax purposes, guaranteed payments are treated as a partner’s distributive share of ordinary income. Guaranteed payments are not subject to income tax withholding. The partnership generally deducts guaranteed payments on Form 1065, line 10, as a business expense. They are also listed on Schedules K and K-1 of the partnership return.

Do you pay self employment tax on partnership income?

Limited partners don’t pay self-employment tax on their distributive share of partnership income, but do pay self-employment tax on guaranteed payments. Additional Information. Instructions for Form 1065, U.S. Return of Partnership Income. Publication 541, Partnerships.

How much income can be split in a partnership?

Section 199A (c) (4) (B) provides however that QBI shall not include any guaranteed payments paid to partners under Section 707 (c). A partnership has $500,000 in net ordinary business income (Line 1 of the Partnership K-1) split between two equal partners at 50 percent each.