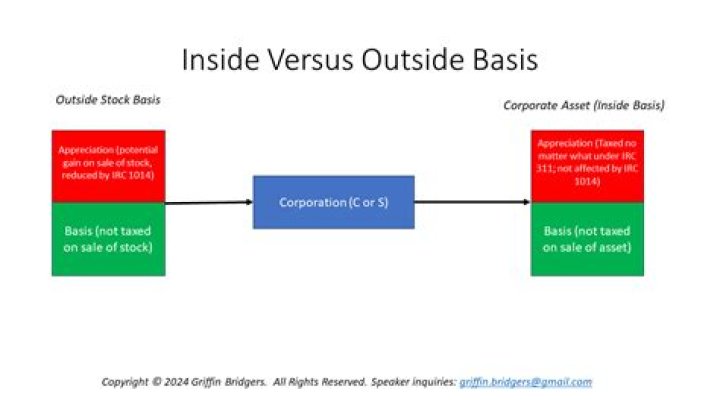

What is outside basis S corporation?

The §1014 basis adjustment applies to the partnership interests and S corporation stock owned by a decedent (the basis in the partnership interests and/or S corporation stock is commonly referred to as the “outside basis”), but not to the assets owned by the partnership or S corporation (the entity’s basis in its …

What is basis for an S Corp?

In computing stock basis, the shareholder starts with their initial capital contribution to the S corporation or the initial cost of the stock they purchased (the same as a C corporation). That amount is then increased and/or decreased based on the pass-through amounts from the S corporation.

What is S Corp basis?

How is S Corp stock basis calculated?

For starters, a shareholder’s stock basis is first calculated by adding their initial capital contribution or the initial cost of the stock they purchased. The stock basis is then increased and/or decreased by items reported on the shareholder’s K-1.

Do you get basis for PPP loan forgiveness?

However, the AICPA noted that while forgiveness of a PPP Loan should create basis that Partnership and S-Corporation owners can use to deduct losses, they ask for clarification for what happens if the expenses are paid in one year, but the loan is not forgiven until a later tax year.

How is stock basis increased in a S corporation?

Assuming no debt basis and using the ordering rules, stock basis is increased by income and reduced by distributions, losses and deductions: ***Since there is adequate stock basis before distribution, the distribution of $16,000 is non-taxable. Shareholders get basis in debt that they personally loan to the S corporation.

When to use the S Corp basis worksheet?

An S corp basis worksheet is used to compute a shareholder’s basis in an S corporation. Shareholders who have ownership in an S corporation must make a point to have a general understanding of basis. The amount that the property’s owner has invested into the property is considered the basis. This basis fluctuates with changes in the company.

Where to find basis on Form 1040 for S corporation?

“ As stated in Part II of the Schedule E (Form 1040), a taxpayer who owns an interest in an S corporation and reports a loss, receives a distribution, disposes of stock, or receives a loan repayment from the S corporation must check a corresponding box under line 28, column (e), and attach a computation detailing their S corporation basis.

How is the outside basis of a partnership calculated?

The calculation of a partner’s outside basis is done by adding and subtracting certain items. Common items that increase a partner’s outside basis are: The increased share of partnership liabilities in the year