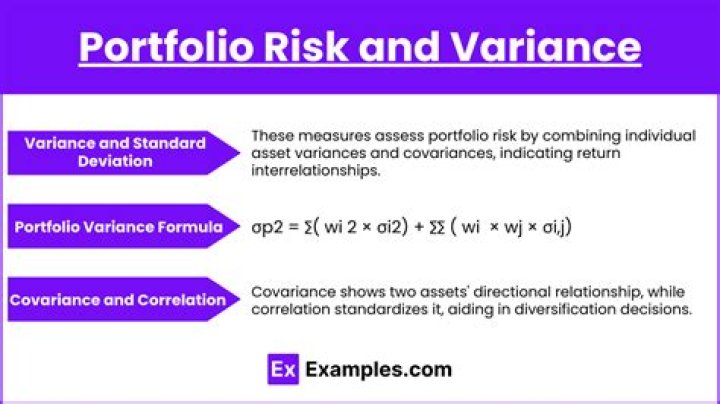

What is portfolio variance formula?

Portfolio variance is calculated by multiplying the squared weight of each security by its corresponding variance and adding twice the weighted average weight multiplied by the covariance of all individual security pairs.

Is high portfolio variance good?

Variance is neither good nor bad for investors in and of itself. However, high variance in a stock is associated with higher risk, along with a higher return. Low variance is associated with lower risk and a lower return. Investors of this kind usually want to have some high-variance stocks in their portfolios.

What is the minimum variance portfolio?

Definition: A minimum variance portfolio indicates a well-diversified portfolio that consists of individually risky assets, which are hedged when traded together, resulting in the lowest possible risk for the rate of expected return.

How do you calculate portfolio VaR?

Steps to calculate the VaR of a portfolio

- Calculate periodic returns of the stocks in the portfolio.

- Create a covariance matrix based on the returns.

- Calculate the portfolio mean and standard deviation (weighted based on investment levels of each stock in portfolio)

How do you find the variance in finance?

Understanding Variance It is calculated by taking the differences between each number in the data set and the mean, then squaring the differences to make them positive, and finally dividing the sum of the squares by the number of values in the data set.

What does it mean if the variance is high?

A large variance indicates that numbers in the set are far from the mean and far from each other. A small variance, on the other hand, indicates the opposite. A variance value of zero, though, indicates that all values within a set of numbers are identical. Every variance that isn’t zero is a positive number.

Is minimum variance portfolio efficient?

The curve connecting such portfolios with minimum variance is called the minimum-variance frontier. As a risk averse investor will only select the portfolio giving higher return for a given level of risk, the part of minimum-variance frontier above the global minimum-variance portfolio is called the efficient frontier.

What does 95% VAR mean?

Risk glossary It is defined as the maximum dollar amount expected to be lost over a given time horizon, at a pre-defined confidence level. For example, if the 95% one-month VAR is $1 million, there is 95% confidence that over the next month the portfolio will not lose more than $1 million.

What is VAR formula?

Value at Risk (VAR) calculates the maximum loss expected (or worst case scenario) on an investment, over a given time period and given a specified degree of confidence. We looked at three methods commonly used to calculate VAR.

What is a high variance?

Variance measures how distant from the mean random values are in a data set. A set of data with low variance (relative) is dominated at the mean, and a set of high variance is spread out and deviates significantly from the mean. A high variance curve will be flat relative to a low variance curve.

Why is my variance so high?

A high variance indicates that the data points are very spread out from the mean, and from one another. Variance is the average of the squared distances from each point to the mean. The process of finding the variance is very similar to finding the MAD, mean absolute deviation.

What does a high variance tell you?

Is high variance good or bad in ML?

High Bias or High Variance This is bad because your model is not presenting a very accurate or representative picture of the relationship between your inputs and predicted output, and is often outputting high error (e.g. the difference between the model’s predicted value and actual value).