What is the accounting treatment of trade discount and cash discount?

Meaning of Cash Discount

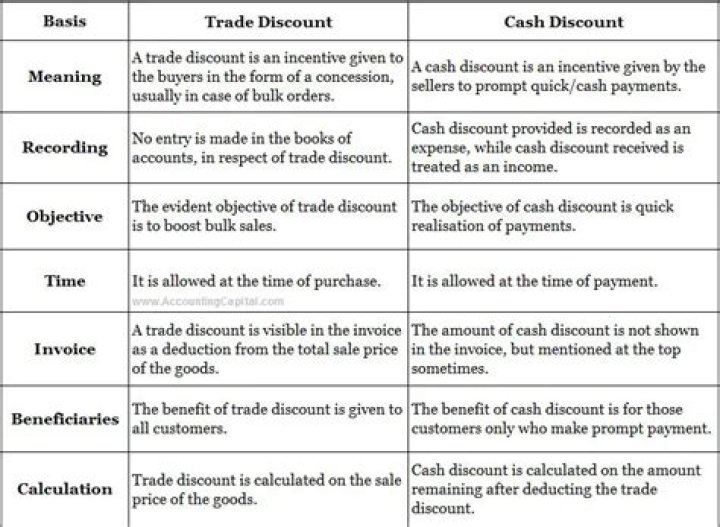

| Basis of Comparison | Trade Discount | Cash Discount |

|---|---|---|

| When discount is allowed | At the time the purchase is made | It is allowed at the time of payment |

| Allowed on transactions | Both cash and credit transactions | Only transactions involving cash payment are allowed. |

How is trade discount treated in accounting?

Accounting for Trade Discounts Trade discounts are deducted outright from the product’s listed price. Meaning, the seller records the sale at the price net of the trade discount. The buyer also records the purchase at net of the trade discount. Trade discount is different from cash discount.

What is the accounting treatment for cash discount?

To record a payment from the buyer to the seller that involves a cash discount, debit the cash account for the amount paid, debit a sales discounts expense account for the amount of the discount, and credit the account receivable account for the full amount of the invoice being paid.

Is cash discount calculated after deducting trade discount?

The invoice price after deducting the trade discount is the starting point of the accounting transaction. The cash discount is only calculated after payment has been made and is therefore the amount is not shown on the invoice.

What is the journal entry for trade discount?

In the case of Trade discount, there is no entry made in the books of accounts of the buyer and seller. It is always deducted before any type of exchange takes place. Hence, it does not form part of the books of accounts of the business. It is usually allowed at the time of purchase.

What is the difference between a trade discount and a cash discount?

Trade Discount is provided to increase sales in bulk quantity, while Cash Discount is given to the customers to encourage early and prompt payment. Trade discount is allowed on both cash and credit transactions. In contrast, a cash discount is allowed to the customers only on cash payments.

How do you use trade discounts?

The trade discount may be stated as a specific dollar reduction from the retail price, or it may be a percentage discount. The trade discount customarily increases in size if the reseller purchases in larger quantities (such as a 20% discount if an order is 100 units or less, and a 30% discount for larger quantities).

How do you account for cash discounts?

In accounting, there are two different ways that cash discounts can be recorded in the books: the net method and the gross method. The net method treats sales revenue as the net amount after the given discount, and any discounts that the buyer doesn’t take are recorded as interest revenue.

How does a trade discount work in accounting?

The company selling the product (and the buyer of the product) will record the transaction at the amount after the trade discount is subtracted. For example, when goods with list prices totaling $1,000 are sold to a wholesaler that is entitled to a 27% trade discount, both the seller and the buyer will record the transaction at $730.

How are cash discounts recorded in the accounting system?

Unlike trade discounts which are not reflected in the accounting system, cash discounts are recorded as “Sales Discount” in the books of the seller and “Purchase Discount” in the books of the buyer under the periodic inventory method.

How are trade discounts recorded in ABC Books?

DEF is granted a 40% trade discount. The entry to record the sale in the books of ABC would be: The amount recorded under “Sales” is at net of the trade discount. The total amount at retail price is $5,000 (i.e. 1,000 x 10 x 0.50). The customer was granted a trade discount of 40%. Hence, sale is recorded at $3,000.

What does it mean to get a cash discount?

Cash discounts are not reductions in the set sales price of a good or service at the time of the transaction – they are a reduction in the amount to be paid by a credit customer (one that is not paying in cash) if that customer pays their debt within a specified time period.