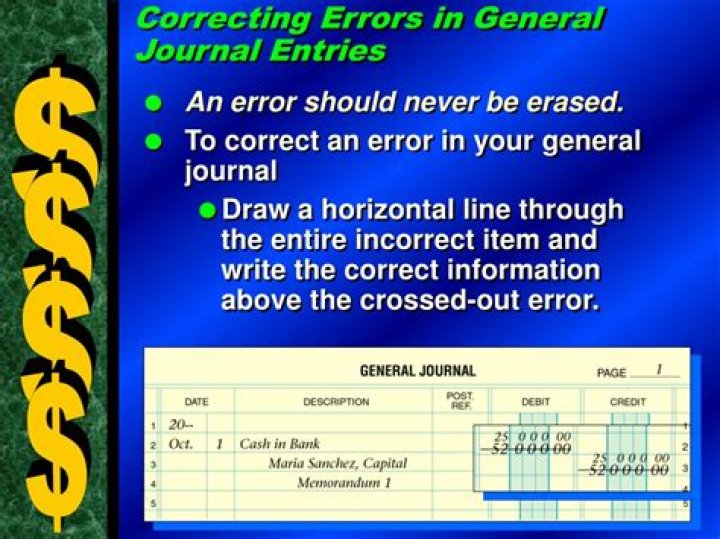

What is the basic rule when correcting accounting errors?

Adding a journal entry may be enough to correct an accounting error. This type of journal entry is called a “correcting entry.” Correcting entries adjust an accounting period’s retained earnings i.e. your profit minus expenses.

How are accounting errors handled?

The best way to correct errors in accounting is to add a correcting entry. A correcting entry is a journal entry used to correct a previous mistake. The type of correcting entry depends on: GAAP (generally accepted accounting practices) guidelines.

What are the accounting requirements when a company finds an error in past reporting?

Accounting rules require a company to disclose error corrections in its annual report for the year in which it made the corrections. The disclosure should describe the nature of the error and the effect of the correction. The corrections do not have to be disclosed in subsequent reports.

How should correction of errors be reported in the financial statements?

How to report an error correction

- Reflect the cumulative effect of the error on periods prior to those presented in the carrying amounts of assets and liabilities as of the beginning of the first period presented; and.

- Make an offsetting adjustment to the opening balance of retained earnings for that period; and.

What is a transposition error in accounting terms?

A transposition error is a data entry snafu that occurs when two digits are accidentally reversed. These mistakes are caused by human error.

What are the categories of accounting changes?

Changes in accounting are of three types. They are changes in accounting principle, changes in accounting estimates, and changes in reporting entity. Accounting errors result in accounting changes too.

What are non-counterbalancing errors?

Non-counterbalancing errors are errors which, if not detected are not automatically counterbalanced or corrected in the next accounting period.In other words, if the net income of one year is understated or overstated, the net income of subsequentyear is not affected.

How do you fix a transposition error in accounting?

How to Correct Transposition Errors. If you find a discrepancy in the accounting records, divide the number by 9. If the error is due to transposition, the number will divide evenly by 9.

What is the accounting treatment for the correction of an error?

When restating the financial statements, follow these three steps: Adjust the balances of any assets or liabilities at the beginning of the newest financial period shown in the comparative statements for the cumulative effect of the error. The other side of the correction goes to retained earnings.

How should a correction of an accounting error be handled and reported in the financial statements?

What are some examples of counterbalancing errors?

An example of a counterbalancing error is expenses charged to year X that should have been charged to year Y. The result is year X has an overstated expense and an understated profit and year Y has an expense understated and the profit overstated.

What is the difference between accounting changes and error correction?

Accounting changes and error correction refers to the guidance on reflecting accounting changes and errors in financial statements. Accounting changes are classified as a change in accounting principle, a change in accounting estimate, and a change in reporting entity.

What is the FASB Statement on accounting changes and error correction?

The FASB’s statement no. 154 addresses dealing with Accounting Changes and Error Correction, while the IASB’s International Accounting Standard 8 “Accounting Policies, Changes in Accounting Estimates and Errors” offers similar guidance.

What are rules for correcting and applying changes to financial statements?

It outlines the rules for correcting and applying changes to financial statements. This includes requirements for the accounting for, and reporting of, a change in accounting principle, change in accounting estimate, change in reporting entity or the correction of a transaction.

What happens when you change the accounting method?

Changing the accounting method used can have dramatic impact on a company’s financial statements. This course covers the accounting, reporting, and disclosures associated with changes in accounting principles (method), estimates, and reporting entities as stipulated in ASC 250-10-05, Accounting Changes and Error Corrections: Overall