What is the cutoff date for Roth IRA contributions?

Contribution limits If you’re still working, review the 2020 IRA contribution and deduction limits to make sure you are taking full advantage of the opportunity to save for your retirement. You can make 2020 IRA contributions until April 15, 2021.

You can make 2020 IRA contributions until April 15, 2021.

Is Roth IRA contribution based on previous year?

You can contribute to a Roth IRA after filing your taxes and you don’t even need to amend your return to do so. The reason the question is there is that you can still contribute to a Roth and count it toward the previous year’s contribution limit—even if you’ve already filed your taxes.

What year did Roth IRA become available?

1998

The Roth IRA, named after the late Delaware Sen. William Roth, became a savings option in 1998, followed by the Roth 401(k) in 2006. Creating a tax-free stream of income is a powerful retirement tool.

Is there a limit on how much you can contribute to a Roth IRA?

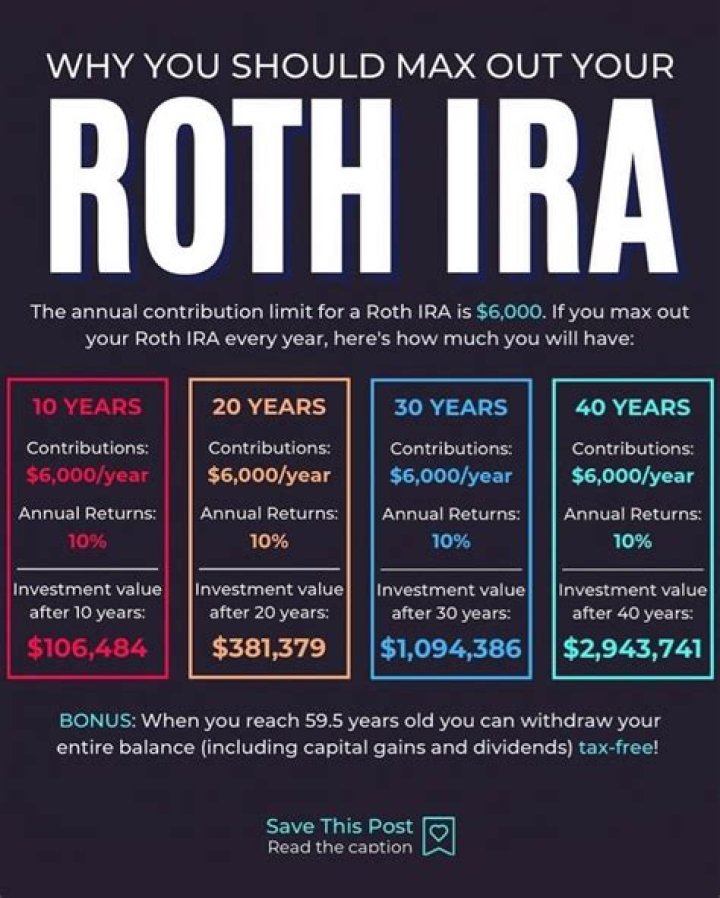

Three Ways to Deal With Contributing Too Much The annual contribution limit to a Roth IRA is $6,000 for 2020 and 2021. Those who are aged 50 and over can contribute an additional $1,000, which is called a catch-up contribution. 2

What happens to excess contributions to a Roth IRA?

The IRS says: “If contributions to your Roth IRA for a year were more than the limit, you can apply the excess contribution in one year to a later year if the contributions for that later year are less than the maximum allowed for that year.” This is referred to as “re-characterizing” an IRA contribution.

What to do if you contribute to a Roth IRA?

If you don’t qualify for a traditional IRA (and thus cannot recharacterize your overage), you can simply withdraw the extra contribution and any NIA. You must do this by the date your tax return is due for that year. 1 3. Apply your contribution to a future year You can also apply the excess contribution and NIA to a future year’s Roth IRA.

Can a business owner contribute to a Roth IRA?

As a business owner, you have an assortment of retirement options. These range from the straightforward, think an Individual or Simple 401 (k), to the more complex, such as a Money Purchase Plan or Profit Sharing. However, for many, the creme de la creme is a Roth IRA.