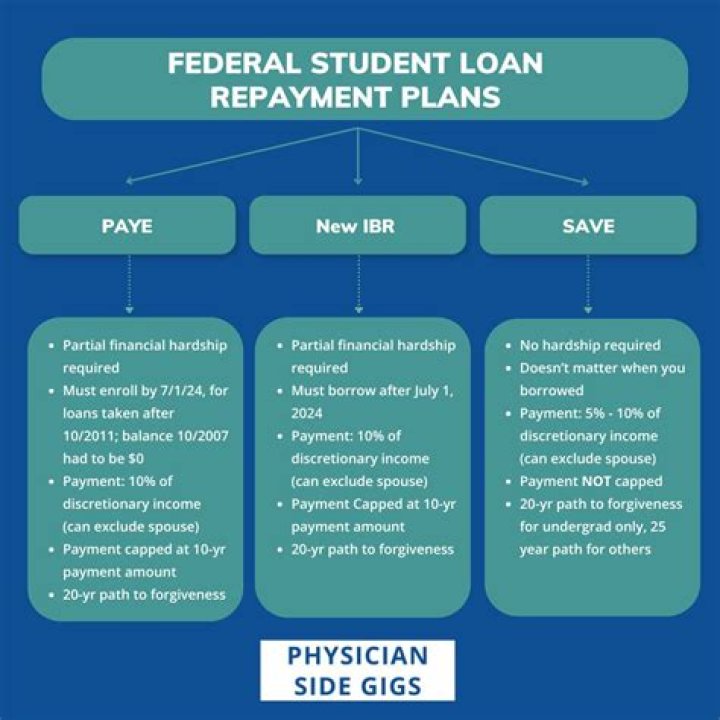

What is the difference between IBR and Repaye?

REPAYE, PAYE, and IBR each have slightly different terms and eligibility restrictions. Additionally, REPAYE does not cap monthly payments at the “standard” repayment amount, as under PAYE and IBR—so as borrowers’ income rises some may face higher monthly payments under REPAYE than PAYE.

Should I recertify my IDR plan?

While you will only need to submit one IDR application to be considered for the IDR plans, you will be required to come back and recertify your income information each year.

What is the best repayment plan for PSLF?

To maximize your PSLF benefit, repay your loans on the Income-Based Repayment (IBR) Plan, the Pay As You Earn Repayment Plan, or the Income Contingent Repayment (ICR) Plan, which are three repayment plans that qualify for PSLF. PSLF is best under IBR, Pay As You Earn, or ICR.

How do I recertify my income based repayment?

Submit your recertification request online at studentloans.gov when your servicer first tells you the deadline. There’s no financial benefit to waiting if you’re worried about rising bills; updated payments don’t go into effect until your previous annual repayment period ends.

What are the pros and cons of an income-based repayment plan for student loans?

Pros and Cons of Income-Driven Repayment Plans for Student Loans

- Pro: Lower monthly payments. This is huge, and the reason many students opt for this plan in the first place.

- Con: Differences between monthly payment/interest.

- Pro: Flexibility.

- Con: Paperwork.

- Pro: Public service forgiveness.

- Con: Forgiven debt is taxed.

How long can you do income based repayment?

The maximum repayment period is 25 years. After 25 years, any remaining debt will be discharged (forgiven). Under current law, the amount of debt discharged is treated as taxable income, so you will have to pay income taxes 25 years from now on the amount discharged that year.