What is the estate exclusion amount?

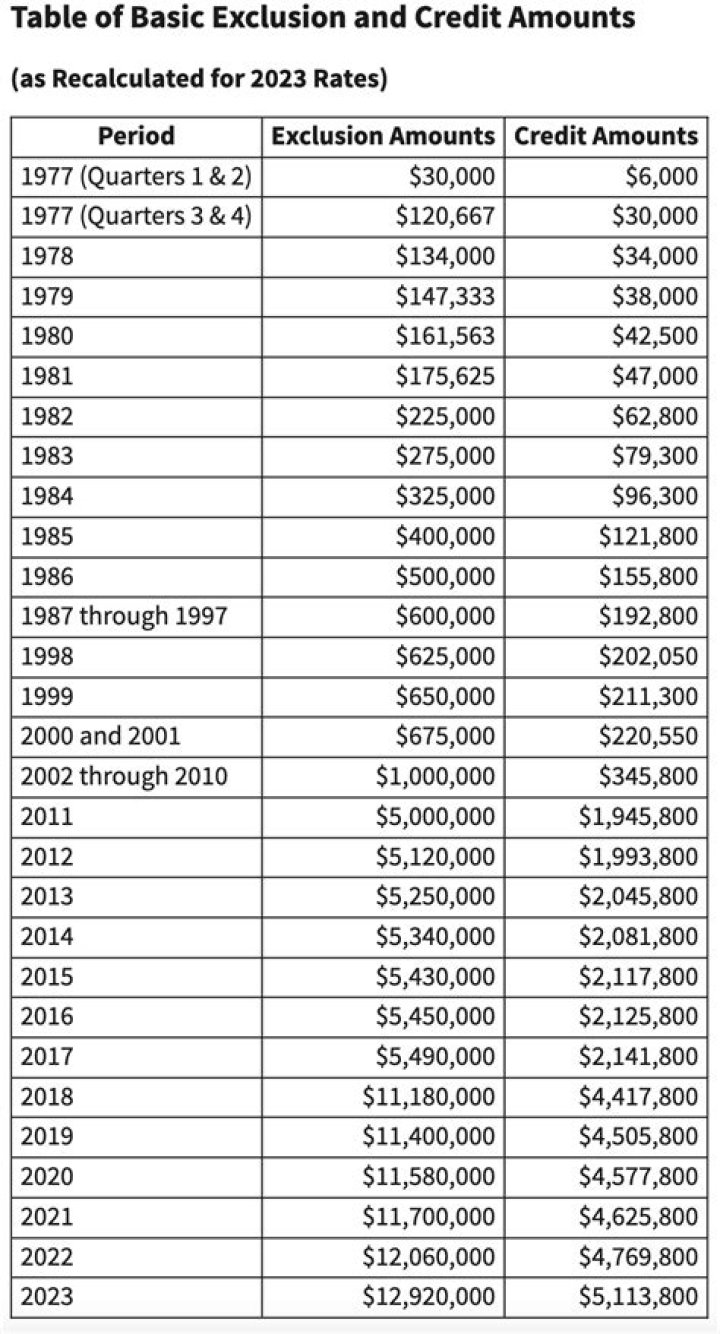

The federal estate tax exemption for 2021 is $11.7 million. The estate tax exemption is adjusted for inflation every year. The size of the estate tax exemption means very few (fewer than 1%) of estates are affected. The current exemption, doubled under the Tax Cuts and Jobs Act, is set to expire in 2026.

Can be elected only if it reduces the value of the gross estate and the estate tax liability?

The election may be made only if it will decrease both the value of the gross estate and the sum (reduced by allowable credits) of the estate tax and the generation-skipping transfer tax payable by reason of the decedent’s death with respect to the property includible in the decedent’s gross estate.

Which is not included in gross estate?

“Gross estate” is a term used to describe the total dollar value of an individual’s assets at the time of their death. A gross estate value does not consider his figure debts owed and tax liabilities.

For 2020, the exemption was $11.58 million per individual, or $23.16 million per married couple. For 2021, an inflation adjustment has lifted it to $11.7 million per individual and $23.4 million per couple. For 2020 and 2021, the top estate-tax rate is 40%. The increase in the exemption is set to lapse after 2025.

What is the estate exclusion for 2019?

In 2018, 2019, 2020, and 2021, the annual exclusion is $15,000.

What are the exclusions from the gross estate?

A. Under Sections 85 and 86, NIRC 1. Capital or exclusive property of the surviving spouse 2. Properties outside the Philippines of a non-resident alien decedent 3. Intangible personal property on the Philippines of a non-resident alien under the Reciprocity Law B. Under Sec. 87, NIRC 1. The merger of usufruct in the owner of the naked title; 4.

What makes up a gross estate for estate tax?

The Gross Estate of a decedent for Federal Estate Tax purposes consists of property falling within the following categories: Property owned by the decedent at his death The main category of property included in a decedent’s gross estate is that in which the decedent had full or partial ownership when he died.

What is the three year rule for gross estate?

The three-year rule also applies to interests in property which would have been included in the gross estate under the above Code sections if the interest had been retained by the decedent. Inclusion of such gifts is required whether or not a gift tax return was required to be filed with respect to the transfer.

What makes up the includible portion of an estate?

The total of all of these items is your “Gross Estate.” The includible property may consist of cash and securities, real estate, insurance, trusts, annuities, business interests and other assets. Keep in mind that the Gross Estate will likely include non-probate as well as probate property.