What is the individual deduction?

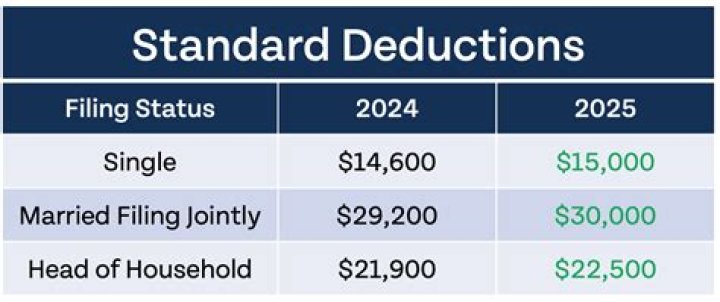

In 2020 the standard deduction is $12,400 for single filers and married filing separately, $24,800 for married filing jointly and $18,650 for head of household. In 2021 the standard deduction is $12,550 for singles filers and married filing separately, $25,100 for joint filers and $18,800 for head of household.

What is individual income Annual?

Annual income is the amount of income you earn in one fiscal year. Your annual income includes everything from your yearly salary to bonuses, commissions, overtime, and tips earned. Gross annual income is your earnings before tax, while net annual income is the amount you’re left with after deductions.

What is a personal deductible contribution?

A personal deductible contribution allows you to reduce your taxable income. The amount of the contribution claimed as a tax deduction is generally taxed at 15%1 (contributions tax) in the fund, instead of your marginal tax rate. Contributions you claim as a tax deduction count as concessional contributions.

Is voluntary super contribution tax deductible?

But thanks to changes in super legislation on 1 July 2017, more Australians are now able to make voluntary tax-deductible, concessional super contributions. If you are self employed you can still do this, but now you’re also eligible if you: Earn salary or wages as an employee. Earn investment income.

Is salary sacrifice a personal contribution?

Salary sacrifice contributions are taxed at a maximum of 15% by your super fund, which is usually less than the tax you pay on income. As you can see below, from a tax and super viewpoint, a personal deductible contribution has the same net effect as salary sacrifice.

Can a contribution to an individual be tax deductible?

Most of the time, contributions to an individual do not qualify as charitable donations, and the IRS does not allow a tax deduction for them.

How much can a corporation deduct for charitable contributions?

A corporation may deduct qualified contributions of up to 25 percent of its taxable income. Contributions that exceed that amount can carry over to the next tax year.

How to calculate your own income tax deduction?

Joe can now compute his own contribution/deduction amount as follows: 1 $100,000 Schedule C net profit 2 – $7,065 ½ SE tax deduction ($14,130 x ½) 3 = $92,935 Net profit reduced by ½ SE tax 4 x 9.0909% Joe’s reduced plan contribution rate 5 = $8,449 Joe’s allowed contribution and deduction

Where do you deduct self employed plan contributions?

Plan contributions for a self-employed individual are deducted on Form 1040, Schedule 1 (on the line for self-employed SEP, SIMPLE, and qualified plans) and not on the Schedule C.