What is the limitation on business interest expense?

The TCJA imposed a limitation for business interest expense based on 30 percent of a taxpayer’s taxable income (with certain adjustments as discussed below). Interest expense that is limited by the 30 percent of adjusted taxable income is suspended and carries forward to subsequent tax years.

What is considered business interest income?

Business interest income means the amount of interest includible in the taxpayer’s gross income for the tax year, which is properly allocable to a trade or business. Business interest income does not include investment income. See C corporation business interest expense and income, later.

Where do I report excess business interest expense?

K-1 reports excess taxable income (ETI) or excess business interest expense (EBIE). Businesses that are subject to section 163(j) must file Form 8990, the IRS form where the 30% limitation is calculated.

When does the business interest expense limitation apply?

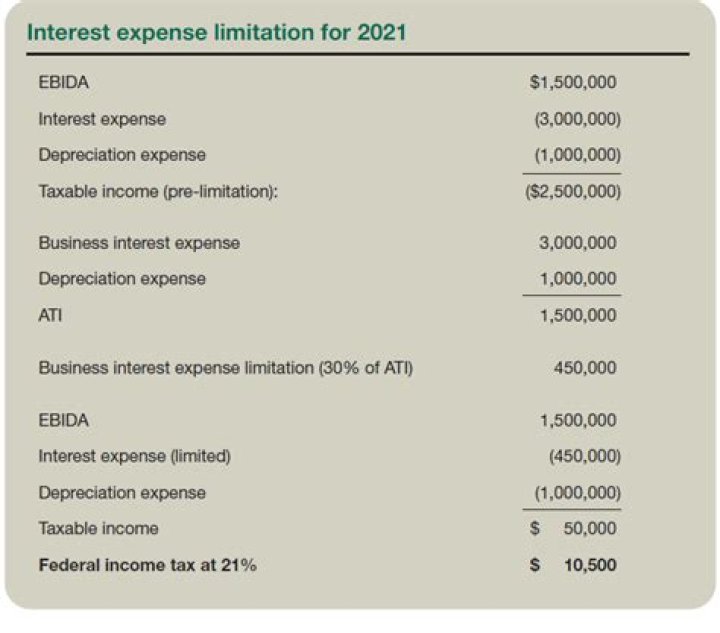

The business interest limitation can have a significant effect on your tax liability and can apply even to conservatively financed businesses. For example, because the limitation is based on a percentage of adjusted taxable income, the limitation can apply in years of low profitability.

What is the 163 ( J ) business interest limitation?

What is the 163 (j) limitation? Code Sec. 163 (j) was added by the Tax Cuts and Jobs Act (TCJA, PL 115-97). It limits the amount of business interest expense that a taxpayer can deduct, effective for tax years beginning after December 31, 2017.

Is there a limitation on the amount of interest you can deduct?

The limitation applies to all business entity types and is generally applied at the entity level. Any interest that is not deductible as a result of the limitation is carried forward indefinitely until it can be absorbed. Subscribe to our communications to get business tips delivered straight to your inbox.

What’s the limit for business interest deduction in 2018?

Effective for tax years starting in 2018, a taxpayer’s deduction for net business interest is limited to 30 percent of adjusted taxable income, which is taxable income without taking into account: The limitation does not apply to investment interest.