What is the minimum capital adequacy ratio under Basel III?

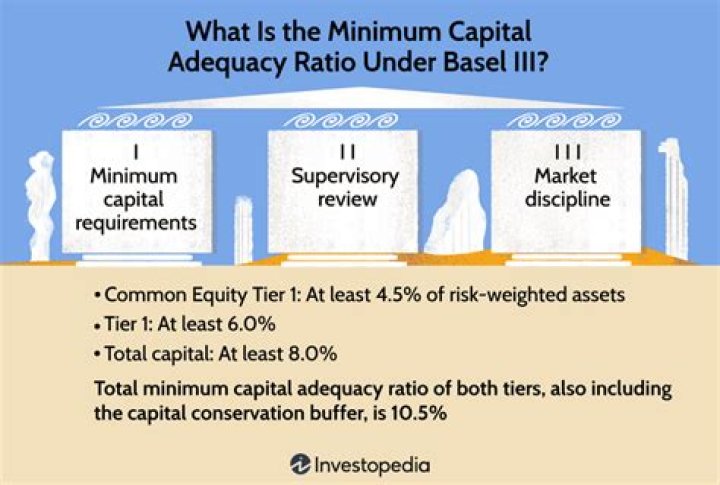

Under Basel III, the minimum capital adequacy ratio that banks must maintain is 8%. The capital adequacy ratio measures a bank’s capital in relation to its risk-weighted assets. The capital-to-risk-weighted-assets ratio promotes financial stability and efficiency in economic systems throughout the world.

What is Liquidity Coverage Ratio (LCR)?

The liquidity coverage ratio (LCR) refers to highly liquid assets held by financial institutions to meet short-term obligations. The ratio is a generic stress test that aims to anticipate market-wide shocks. The LCR assures that financial institutions have the necessary assets on hand to ride out any short-term liquidity disruptions.

What is a Statutory Liquidity Ratio?

Statutory Liquidity Ratio refers to the amount that the commercial banks require to maintain in the form of cash, or gold or govt. approved securities before providing credit to the customers.

How to calculate a bank’s liquidity position?

Understanding Bank Liquidity. Before you get started,fully understand the information you’re trying to extract.

What are the differences between Basle 1, 2 and 3?

The key difference between Basel 1 2 and 3 is that Basel 1 is established to specify a minimum ratio of capital to risk-weighted assets for the banks whereas Basel 2 is established to introduce supervisory responsibilities and to further strengthen the minimum capital requirement and Basel 3 to promote the need for liquidity buffers (an additional

What is meant by Basel norms in banking?

BASEL Norms are the standards issued by the Basel Committee on Banking Supervision (BCBS) to strengthen the international banking system.

What is Basel in banking?

What is ‘Basel I’. Basel I is a set of international banking regulations put forth by the Basel Committee on Bank Supervision ( BCBS ) that sets out the minimum capital requirements of financial institutions with the goal of minimizing credit risk.