What is the retail method of estimating inventory?

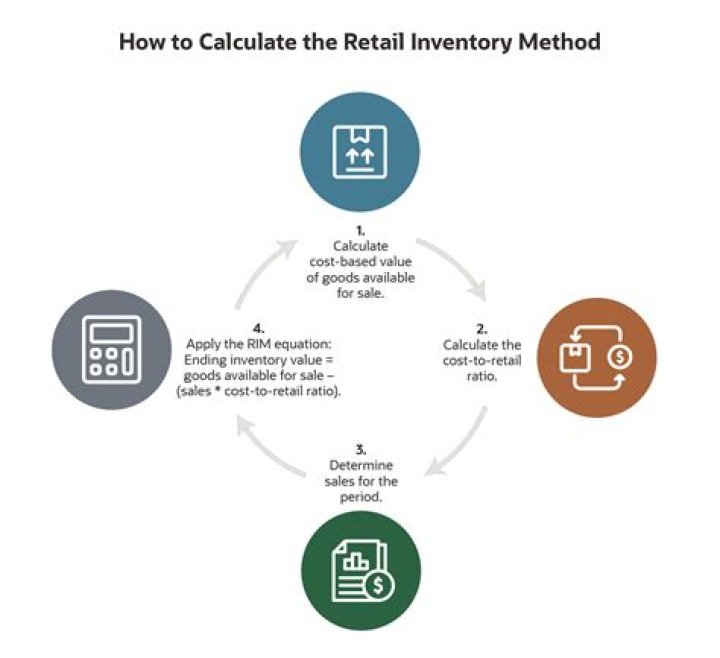

The Retail Inventory Method is an accounting procedure used to estimate the value of a store’s inventory over time. It works by first taking the total retail value of all the products you have in your inventory, then subtracting the total amount of sales, then multiply that amount by the cost-to-retail ratio.

Who uses the retail inventory method?

The retail inventory method is used by retailers that resell merchandise to estimate their ending inventory balances. This method is based on the relationship between the cost of merchandise and its retail price.

What is the cost-to-retail ratio using the retail method?

Divide the cost of goods available for sale by the retail price of goods available for sale to calculate your cost-to-retail ratio, or percentage. In this example, divide $80,000 by $160,000 to get 0.5, or 50 percent.

On what assumption is the retail inventory method based?

weighted average cost flow assumption

Retail Inventory Method The retail method can be used with FIFO, LIFO, or the weighted average cost flow assumption. It is based on the (known) relationship between cost and retail prices of inventory. In addition it is used in conjunction with the dollar value LIFO method.

What are benefits of the retail inventory method and how is it applied?

One advantage of the retail method of inventory is that is produces solid inventory control records. It ties the direct products to the sales and provides an ending count without much additional work. It deals directly with items and not lots or groupings of items.

Why do companies use a cost-to-retail ratio?

Calculating Ending Retail Inventory The cost-to-retail ratio, also called the cost-to-retail percentage, provides how much a good’s retail price is made up of costs.

The retail method can be used with FIFO, LIFO, or the weighted average cost flow assumption. It is based on the (known) relationship between cost and retail prices of inventory. In addition it is used in conjunction with the dollar value LIFO method.

What was Henke’s inventory at July 31, 2010?

Henke Co. uses the retail inventory method to estimate its inventory for interim statement purposes. Data relating to the computation of the inventory at July 31, 2010, are as follows: a. $72,000.

What should inventory be reported at under lower of cost or market?

As a result, under the lower-of-cost-or-market method, the inventory item should be reported at the a. net realizable value. b. net realizable value less the normal profit margin.

What was Ryan Distribution Co’s inventory at December 31, 2010?

Ryan Distribution Co. has determined its December 31, 2010 inventory on a FIFO basis at $250,000. Information pertaining to that inventory follows: Ryan records losses that result from applying the lower-of-cost-or-market rule. At December 31, 2010, the loss that Ryan should recognize is

What is the net realizable value of inventory?

The original cost of an inventory item is above the replacement cost and the net realizable value. The replacement cost is below the net realizable value less the normal profit margin. As a result, under the lower-of-cost-or-market method, the inventory item should be reported at the a. net realizable value.