What is the Section 1245 recapture rule?

Section 1245 is a mechanism to recapture at ordinary income tax rates allowable or allowed depreciation or amortization taken on section 1231 property. Allowable or allowed means that the amount of depreciation or amortization recaptured is the greater of that taken or that could have been taken but was not.

Do you have to recapture depreciation on 1245 property?

When a business or real estate investment is sold, 1245 property that was depreciated must be recaptured. The recaptured depreciation is taxed as ordinary income up to one of the following: The allowed or allowable depreciation or amortization on the property.

How is 1245 depreciation recapture calculated?

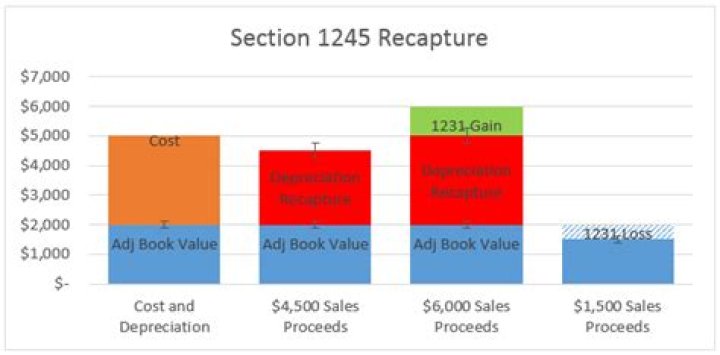

Section 1245 Depreciation Recapture For example, if business equipment was purchased for $10,000 and had a depreciation expense of $2,000 per year, its adjusted cost basis after four years would be $10,000 – ($2,000 x 4) = $2,000.

How do you bypass depreciation recapture?

Luckily, you can avoid depreciation recapture tax on a rental property. One of the best methods is to use a 1031 exchange. Using a 1031 exchange enables investors to defer most, if not all, of their depreciation recapture tax, not to mention their capital gains tax.

Is Section 1245 recapture ordinary income?

If you sell Section 1245 property, you must recapture your gain as ordinary income to the extent of your earlier depreciation deductions on the asset that was sold. Any gain up to the amount of the previously taken depreciation will be taxed at ordinary income rates.

Can you avoid depreciation recapture?

Exchange to avoid recapture Another way to avoid depreciation recapture is by selling the property for less than its book value, which wouldn’t make much sense. Another solution is to hold onto the asset until you die. A non-recognized gain avoids the depreciation recapture trigger.

How is depreciation recapture calculated?

Subtract the taken or allowable depreciation expense from your original cost basis. This amount is your adjusted cost basis. For example, if you paid $10,000 for a tractor and took $4,000 in depreciation expenses, your new adjusted cost basis would be $10,000 minus $4,000, or $6,000.

How is recapture calculated?

Start with your UCC in any class and add the amount you spent on new property in the class. Then, subtract the proceeds you earned from the disposition of property in that class.

What is the depreciation recapture tax rate for 2020?

25%

Depreciation recapture is the portion of your gain attributable to the depreciation you took on your property during prior years of ownership, also known as accumulated depreciation. Depreciation recapture is generally taxed as ordinary income up to a maximum rate of 25%.

Can I avoid depreciation recapture?

What is a Section 1245 property?

According to the Internal Revenue Service (IRS), Section 1245 property is defined as intangible or tangible personal property that could be or is subject to depreciation or amortization, excluding buildings (real estate) and structural components.

How is 1245 recapture calculated?

What are examples of 1245 property?

A few examples of 1245 property are: furniture, fixtures & equipment, carpet, decorative light fixtures, electrical costs that serve telephones and data outlets.

What is the difference between Section 1231 and 1245 property?

Section 1231 property are assets that are used in your trade or business and are held by the Taxpayer for more than one year. If you sell Section 1245 property, you must recapture your gain as ordinary income to the extent of your earlier depreciation deductions on the asset that was sold.

Is a vehicle 1231 or 1245 property?

Specifically, section 1245 property examples include all depreciable and tangible personal property, such as furniture and equipment, or other intangible personal property, such as a patent or license, which is subject to amortization. Automobiles fall into the Section 1245 asset category.

What happens if I don’t depreciate my rental property?

However, not depreciating your property will not save you from the tax – the IRS levies it on the depreciation that you should have claimed, whether or not you actually did. With this in mind, depreciating your property doesn’t hurt you when you sell it, but it really helps you while you own it.

What is the difference between 1245 and 1231 property?

What kind of gain is sale of rental property?

Taxes Rental Property Investors Need to Pay When you sell a rental property, you need to pay tax on the profit (or gain) that you realize. The IRS taxes the profit you made selling your rental property two different ways: Capital gains tax rate of 0%, 15%, or 20% depending on filing status and taxable income.