What is the slope of security market line?

The slope of the security market line represents the market risk premium, i.e. the excess return over the market return. The market risk premium compensates for the additional systematic risk associated with the security.

Can the security market line have a negative slope?

The two curves are equivalent only if (i.e., portfolio i is perfectly correlated with the market portfolio); if , and E(Ri) is equal, the CML has a higher slope with respect to the SML; with , the SML will have a negative slope. …

How do you read a security market line?

The two-dimensional correlation between expected return and beta can be calculated through the CAPM formula and expressed graphically through a security market line, or SML. Any security plotted above the SML is interpreted as undervalued. A security below the line is overvalued.

Is beta the slope of the security market line?

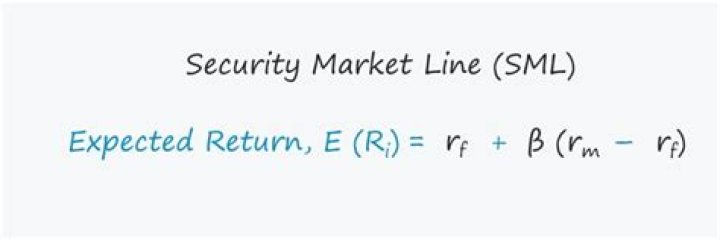

Beta (slope) is an essential measure in the Security Market Line equation. If Beta = 1, then the stock has the same level of risk as to the market. A higher beta, i.e., greater than 1, represents a riskier asset than the market, and beta less than 1 represents risk less than the market.

What security market line tells us?

Security market line (SML) is the representation of the capital asset pricing model. It displays the expected rate of return of an individual security as a function of systematic, non-diversifiable risk. The risk in these individual risky securities reflects the systematic risk.

What is the slope of the security market line quizlet?

The slope of the SML, which is the difference between the expected return on a market portfolio and the risk-free rate. In other words, it is the reward investors expect to earn for holding a portfolio of beta of 1. The equation of the SML showing the relationship between expected return and beta.

What is the difference between capital market line and security market line?

Capital Market Line is a theoretical concept that represents all the portfolios that optimally combine the risk-free rate of return and the market portfolio of risky assets. Security Market Line measures the risk through beta, which helps to find the security’s risk contribution to the portfolio.

How is capital market line calculated?

The Capital Market Line (CML) formula can be written as follows:

- ERp = Rf + SDp * (ERm – Rf) /SDm

- Suppose that the current risk-free rate is 5%, and the expected market return is 18%.

- Calculation of Expected Return of Portfolio A.

- Calculation of Expected Return of Portfolio B.

What is the slope of the capital allocation line?

The slope of the capital allocation line is equal to the incremental return of the portfolio to the incremental increase of risk.

Which of the following is the best definition of security market line?

The security market line (SML) is a line drawn on a chart that serves as a graphical representation of the capital asset pricing model (CAPM)—which shows different levels of systematic, or market risk, of various marketable securities, plotted against the expected return of the entire market at any given time.

What is the security market line quizlet?

Definition of SML. The line that reflects the relationship between systematic risk and return available for all risky assets in the capital market at a given time.

What is the equation of Bo’s capital allocation line?

What is the equation of Bo’s capital allocation line? The intercept is the risk-free rate (3.60%) and the slope is (12.00% – 3.60%)/7.20% = 1.167.

What does security market line mean?

How do we calculate the expected return on a security?

Expected return is calculated by multiplying potential outcomes (returns) by the chances of each outcome occurring, and then calculating the sum of those results (as shown below).