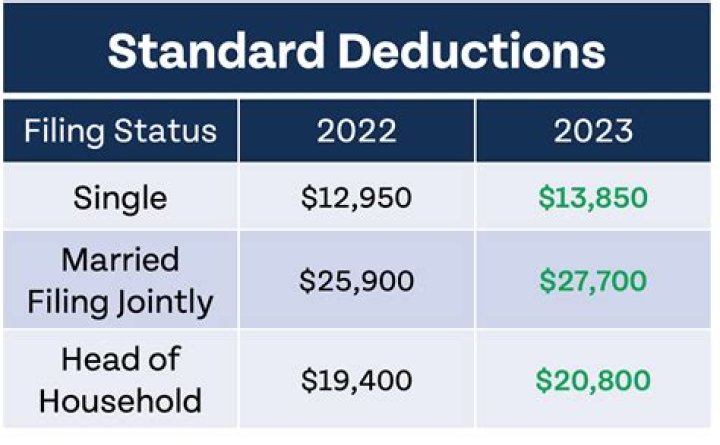

What is the South Carolina standard deduction?

The standard deduction, which South Carolina has, is a deduction that is available by default to all taxpayers who do not instead choose to file an itemized deduction. Essentially, it translates to $12,000.00 per year of tax-free income for single South Carolina taxpayers, and $24,000.00 for those filing jointly.

Does South Carolina allow capital loss carryforward?

(J) A net operating loss carryforward under Section 12-7-705 as in effect on December 31, 1984, is allowed for South Carolina income tax purposes before loss carryforwards pursuant to the Internal Revenue Code Section as modified by Article 9 of this chapter, but the same loss may not be deducted more than once.

What are the tax rates in South Carolina?

South Carolina’s general state Sales and Use Tax rate is 6%. In certain counties, local Sales and Use Taxes are imposed in addition to the 6% state rate.

How are capital gains taxed in South Carolina?

Capital gains are taxed at two different levels in South Carolina. First, short-term capital gains (those realized in less than a year) are considered normal taxable income and taxed at the rates, up to 7%, listed above. For long-term gains, 44% of the “net capital gain” is exempt.

How much can I deduct from my South Carolina taxes?

If you are age 65 or older, you may claim a deduction of up to $10,000. An individual taxpayer who has military retirement income, each year may deduct an amount of his South Carolina earned income from South Carolina taxable income equal to the amount of military retirement income that is included in South Carolina taxable income.

What’s the tax rate on cigarettes in South Carolina?

For long-term gains, 44% of the “net capital gain” is exempt. The net capital gain is the net long-term gain (of more than a year) minus any short-term loss for the taxable year. The South Carolina cigarette tax is just 57 cents per pack of 20. That’s the seventh-lowest rate in the country.

Do you pay taxes on property sold in South Carolina?

You do not pay taxes in this state on property sold in another state. A deduction of 44% is allowed on net long-term capital gains. The South Carolina holding period for long-term gains is the same as the federal. You may deduct a portion of your qualified retirement income included in South Carolina taxable income.