What qualifies as MACRS property?

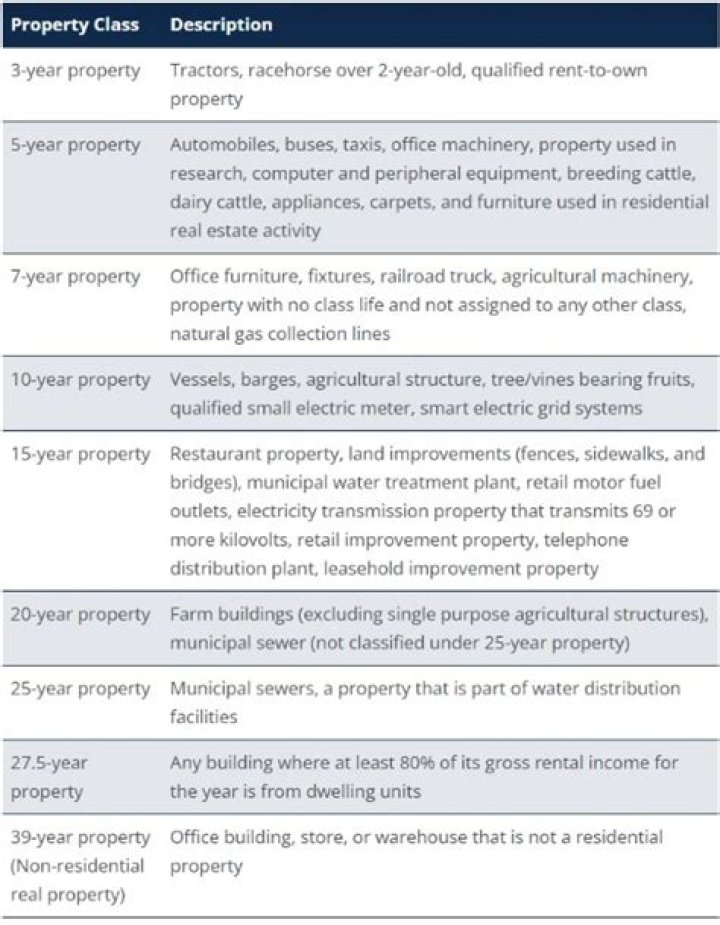

Any building or structure where 80% or more of its gross rental income is from dwelling units. 27.5. An office building, store, or warehouse that is not residential property or has a class life of less than 27.5 years. 39. This information is provided by the IRS.

Which is not an allowable method under MACRS?

The modified accelerated cost recovery system (MACRS) is the current tax depreciation system. The sum of the years digits is not an allowable method under MACRS.

Which of the following can be depreciated for tax purposes?

You can depreciate most types of tangible property (except land), such as buildings, machinery, vehicles, furniture, and equipment. You can also depreciate certain intangible property, such as patents, copyrights, and computer software. To be depreciable, the property must meet all the following requirements.

How is MACRS depreciation calculated?

In MACRS straight line, LN calculates the percentage for a year by dividing one depreciation period by the remaining life of the asset, and then applying this amount with the averaging convention to determine the depreciation amount for that year.

Is Macrs acceptable under GAAP?

Income Tax Depreciation is not GAAP Depreciation The Modified Accelerated Cost Recovery System (MACRS), depreciation schedules for income tax reporting only.

What is the depreciation life of a rental property?

By convention, most U.S. residential rental property is depreciated at a rate of 3.636% each year for 27.5 years. Only the value of buildings can be depreciated; you cannot depreciate land.

What items should be depreciated?

Examples of Depreciating Assets

- Manufacturing machinery.

- Vehicles.

- Office buildings.

- Buildings you rent out for income (both residential and commercial property)

- Equipment, including computers.

Is accelerated depreciation allowed under GAAP?

Accelerated depreciation rates acceptable to GAAP are based on the estimated life of the asset and also follow the matching principle. The larger depreciation expense in the early years is matched with the greater revenue generated when the equipment is newer and more efficient, and generating the most income.