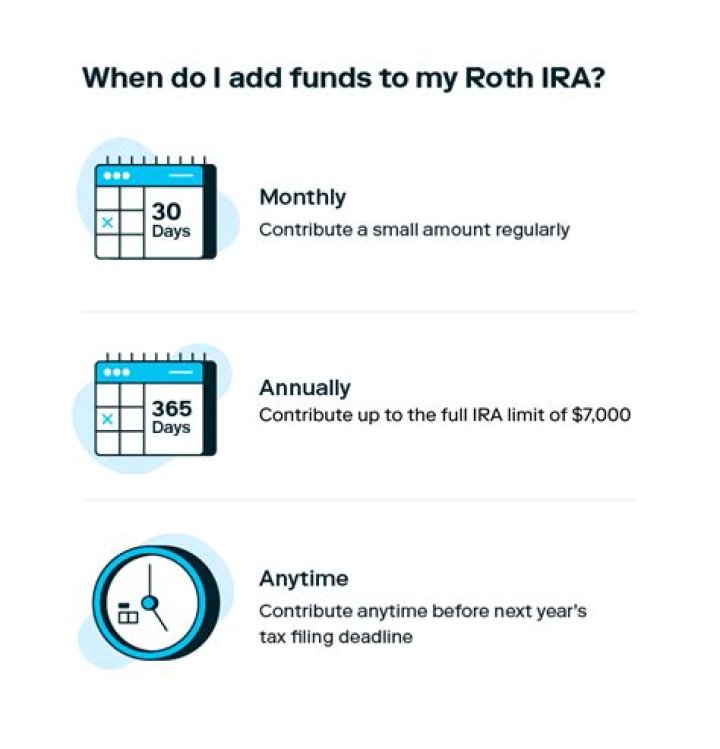

When can you add more to your Roth IRA?

Only earned income can be contributed to a Roth IRA. You can contribute to a Roth IRA only if your income is less than a certain amount. The maximum contribution for 2021 is $6,000; if you’re age 50 or over, it is $7,000. You can withdraw contributions tax-free at any time, for any reason, from a Roth IRA.

Does the 5-year rule apply to Roth rollover?

It is possible to roll over or transfer Roth IRA funds to another Roth IRA. The 5-year rule for qualified distributions of earnings from a Roth starts with your first Roth IRA contribution or conversion. It does not restart when funds are moved to another Roth IRA.

When does the five year clock start on a Roth IRA?

The five-year rule has to do with qualified distributions of earnings, which is not the case here. However, all is not lost. With a Roth IRA conversion, the five-year clock begins on January 1 of the year you converted.

When to convert a traditional IRA to a Roth IRA?

As with contributions, the five-year rule for Roth conversions uses tax years, but the conversion must occur by Dec. 31 of the calendar year. 6 For instance, if you converted your traditional IRA to a Roth IRA in Nov. 2019, your five-year period begins Jan. 1, 2019.

When do you take money out of a Roth IRA?

However, all is not lost. With a Roth IRA conversion, the five-year clock begins on January 1 of the year you converted. So if you converted to a Roth in December of 2015, for example, your Roth IRA by early 2017 would be two years into the five-year wait before earnings can be withdrawn tax free.

Is there an exception to the 5 year rule in a Roth IRA?

Death is also an exception. When a Roth IRA owner dies, beneficiaries who inherit the account can take a distribution without incurring a penalty—no matter whether the distribution is principal or earnings. 7 However, death does not totally get you off the hook of the five-year rule.