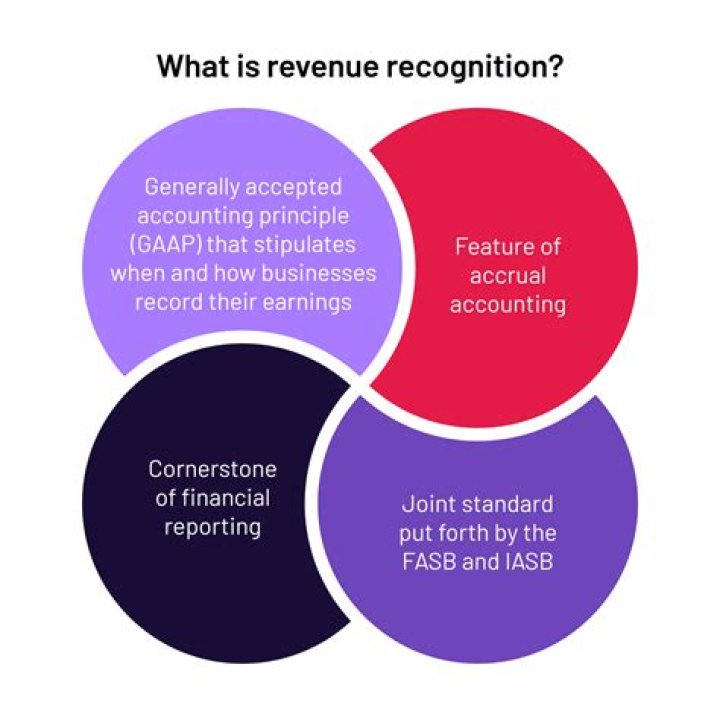

When should a company recognize revenue on its books?

According to generally accepted accounting principles (GAAP), the following two criteria must be satisfied before the company can record revenue on its books: A critical event must trigger the transaction process. The money resulting from the transaction must be measurable within a certain degree of reliability.

Should revenue be recorded early?

By recording revenue early, a dishonest business seller or an employee under pressure to meet financial benchmarks can significantly distort profits.

When should you record revenue?

Revenue should be recorded when the business has earned the revenue. This is a key concept in the accrual basis of accounting because revenue can be recorded without actually being received. Revenues are realized or realizable when a company exchanges goods or services for cash or other assets.

Is the key to Recognising revenue correctly?

The revenue is recognized: At the gross amount charged. The cost of goods sold reflects the cost of the goods or services sold to the customer plus the company’s cost of executing the transaction. At the net amount (reflecting only the commission or net profit).

According to the principle, revenues are recognized when they are realized or realizable, and are earned (usually when goods are transferred or services rendered), no matter when cash is received. In cash accounting – in contrast – revenues are recognized when cash is received no matter when goods or services are sold.

How do you record revenue recognition?

Recognizing Revenue at Point of Sale or Delivery The accrual journal entry to record the sale involves a debit to the accounts receivable account and a credit to the sales revenue account; if the sale is for cash, the cash account would be debited instead.

What is the difference between bookings and revenue?

‘ It indicates the value of a contract signed with a prospective customer for a given period of time. For a particular month, your bookings comprise the sum of all deals closed in that month. Revenue is the actual income earned when you deliver on the promised service to your customers.

When do you need to recognize revenue for tax purposes?

Section 451 (b) (1) generally provides that an accrual method taxpayer with an applicable financial statement (AFS) or other specified financial statement is required to recognize revenue for tax purposes no later than when such revenue has been recognized as revenue in an AFS or other specified financial statement.

What does the new revenue recognition standard mean for tax?

If the taxpayer is currently following the financial accounting method to recognize revenue and that method is not permissible for tax purposes, it should change to a permissible method of accounting under Sec. 460, which would create a book-tax difference related to revenue recognition.

Can a company change its accounting method for revenue recognition?

Additionally, a company cannot simply change its tax method of accounting for revenue recognition without requesting IRS consent on Form 3115, Application for Change in Accounting Method.

How does the earlier of test affect income taxes?

The new earlier of test affects the timing of when gross income is recognized for tax purposes. This can lead to different conclusions on the need for a deferred tax asset or liability based on why financial statement revenue is earlier. The following summarizes two of the illustrative examples in the Blue Book.