Where are intangibles listed on the balance sheet?

Intangible assets are generally both nonphysical and noncurrent; they appear in a separate long-term section of the balance sheet entitled “Intangible assets”. Initially, firms record intangible assets at cost like most other assets.

Does intangible assets have a debit or credit balance?

You credit your intangible asset account because it is an asset. Assets are also increased by debit and decreased by credit. You are increasing your expenses and decreasing your assets through the amortization process.

Is an example of intangible assets?

An intangible asset is an asset that is not physical in nature. Goodwill, brand recognition and intellectual property, such as patents, trademarks, and copyrights, are all intangible assets. Intangible assets exist in opposition to tangible assets, which include land, vehicles, equipment, and inventory.

Why are intangible assets listed on the balance sheet?

Intangible asset that are listed on a company’s balance sheet should be those of an acquired asset. They have an identifiable value, a useful lifespan and appropriate amortisation policies could be adopted to amortise these assets over different lifecycles. Unfortunately, the current accounting standards tends to overlook internally-created assets.

Which is an example of a tangible asset?

Examples are goodwill, patents, trademarks, and copyrights. A tangible Asset has a physical nature and can include buildings, vehicles, equipment, and stock. They are typically listed on the balance sheet as part of the assets of the business.

How much does Apple have in intangible assets?

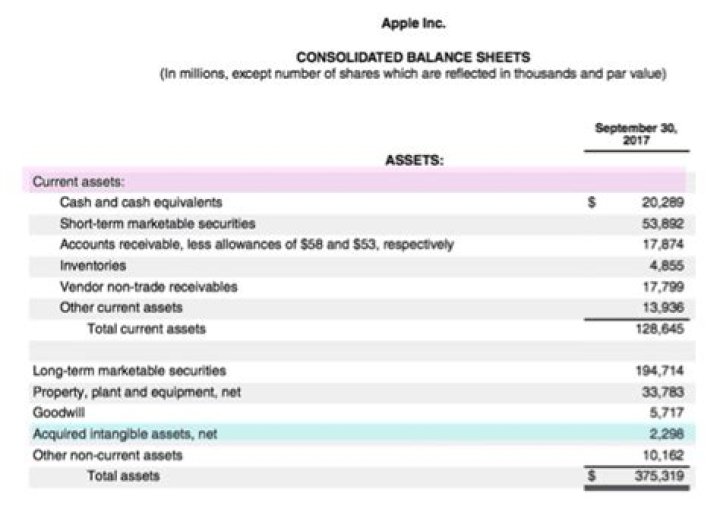

Intangible assets were approximately $2.2 billion for Apple in 2017 (highlighted in blue). Intangible assets are not listed under current assets (in pink) showing their long-term useful life.

What makes an asset an asset on a balance sheet?

It is a generally accepted that any asset listed on a company’s balance sheet should have an identifiable fair value attached to it. Hence, if data is to be considered as an asset, there must be a corresponding cost for acquiring or building this asset.