Where do fringe benefits go on tax return?

Any fringe benefit provided to an employee is taxable income for that person unless the tax law specifically excludes it from taxation. Taxable fringe benefits must be included as income on the employee’s W-2 and are subject to withholding.

How does fringe benefit affect tax return?

Consequences of having a reportable fringe benefits amount Even though a reportable fringe benefits amount (RFBA) is included on your income statement or payment summary and is shown on your tax return, you do not: include it in your total income or loss amount. pay income tax or Medicare levy on it.

Do you have to report de minimis?

How are de minimis fringe benefits reported? If the benefits qualify for exclusion, no reporting is necessary. If they are taxable, they should be included in wages on Form W-2 and subject to income tax withholding.

What does the IRS considered de minimis?

An essential element of a de minimis benefit is that it is occasional or unusual in frequency. It also must not be a form of disguised compensation. The IRS has ruled previously in a particular case that items with a value exceeding $100 could not be considered de minimis, even under unusual circumstances.

What fringe benefits are excluded from taxes?

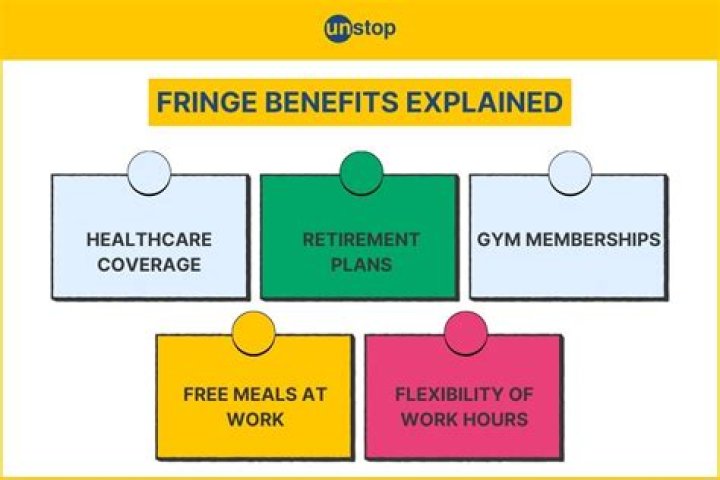

Other fringe benefits that are not considered taxable to employees include health insurance (up to a maximum dollar amount), dependent care, group term-life insurance, qualified benefits plans such as profit sharing or stock bonus plans, commuting or transportation benefits, employee discounts, and working condition …

What is the tax treatment for de minimis benefits?

Many benefits provided by employers are taxable as income to the employees, but a de minimis benefit is not. From a tax standpoint, a de minimis benefit is a small amount of employee compensation, and Internal Revenue Code section 132(a)(4) states that these small amounts are not subject to taxation.

Is the de minimis rule applicable to fringe benefits?

Consider the application of the de minimis rule (which allows unclassified fringe benefits of up to $300 per employee per quarter and $22,500 to all employees over the previous four quarters to be exempt from FBT); can you manage your fringe benefits to fall within these rules? Are you attributing fringe benefits to your employees?

How much can a company deduct for fringe benefits?

The IRS does not specify a maximum dollar amount for excluding de minimis fringe benefits from an employee’s taxable income, but the business can deduct no more than $25 of a gift to any one person each year, including employees.

When is cash not considered a de minimis benefit?

The IRS has ruled previously in a particular case that items with a value exceeding $100 could not be considered de minimis, even under unusual circumstances. Cash is generally intended as a wage, and usually provides no administrative burden to account for. Cash therefore cannot be a de minimis fringe benefit.

How are de minimis benefits excluded from Internal Revenue Code?

De minimis benefits are excluded under Internal Revenue Code section 132(a)(4) and include items which are not specifically excluded under other sections of the Code. These include such items as: De Minimis Fringe Benefits | Internal Revenue Service Skip to main content An official website of the United States Government English