Which of the following is true regarding traditional IRAs?

All of the following are true regarding traditional IRAs, EXCEPT: An IRA may be deducted from gross income up to the annual contribution limit. Interest earned on IRA contributions is tax-deferred until withdrawn. The correct answer is: Interest earned on IRA contributions is taxable in the year earned.

Which of the following are rules of the traditional IRA?

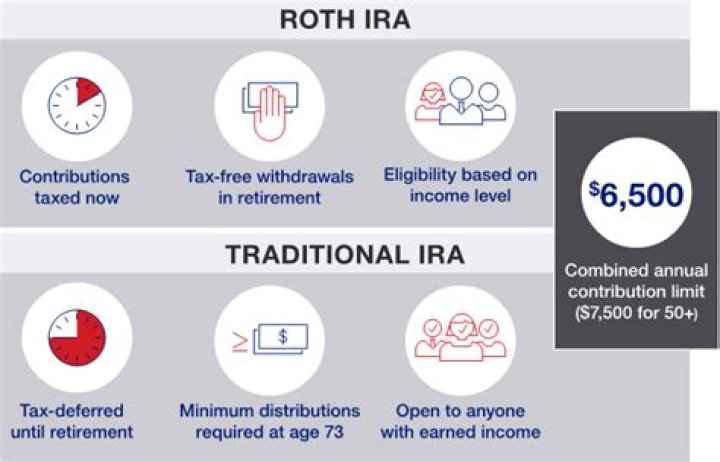

Quick summary of IRA rules The maximum annual contribution limit is $6,000 in 2021 ($7,000 if age 50 or older). Contributions may be tax-deductible in the year they are made. Investments within the account grow tax-deferred. Withdrawals in retirement are taxed as ordinary income.

How does traditional IRA work?

An individual retirement account (IRA) allows you to save money for retirement in a tax-advantaged way. Traditional IRA – You make contributions with money you may be able to deduct on your tax return, and any earnings can potentially grow tax-deferred until you withdraw them in retirement.

Which of the following descriptions of a regular rollover from a qualified plan to a traditional IRA is correct?

Which of the following descriptions of a regular rollover from a qualified plan to a traditional IRA is CORRECT? Mandatory withholding of 20% for federal income tax applies in the event of the employee-participant’s physical possession of the amount rolled over.

What qualifies an individual to contribute to an IRA?

Almost anyone can contribute to a traditional IRA, provided you (or your spouse) receive taxable income and you are under age 70 ½. SIMPLE and SEP IRAs are for self-employed individuals or small business owners. To set up a SIMPLE IRA an employer must have 100 or fewer employees earning more than $5,000 each.

Which of the following is an acceptable investment for an IRA?

Almost any type of investment is permissible inside an IRA, including stocks, bonds, mutual funds, annuities, unit investment trusts (UITs), exchange-traded funds (ETFs), and even real estate.

Does traditional IRA have income limits?

There are no income limits for Traditional IRAs,1 however there are income limits for tax deductible contributions. There are income limits for Roth IRAs. A partial contribution is allowed for 2021 if your modified adjusted gross income is more than $125,000 but less than $140,000.

How do I prove a rollover?

Look for Form 1099-R in the mail from your plan administrator at the end of the year. Your rollover is reported as a distribution, even when it is rolled over into another eligible retirement account. Report your gross distribution on line 15a of IRS Form 1040. This amount is shown in Box 1 of the 1099-R.

Can I hold individual stocks in my IRA?

IRAs allow you to choose from individual securities, such as stocks, bonds, certificates of deposit (CDs), exchange-traded funds (ETFs), or a “single-fund” option.

Do you pay taxes on gains in a traditional IRA?

More In Retirement Plans A traditional IRA is a way to save for retirement that gives you tax advantages. Generally, amounts in your traditional IRA (including earnings and gains) are not taxed until you take a distribution (withdrawal) from your IRA.

Can I contribute to traditional IRA with high income?

If a high-income earner decides to make an IRA contribution, the contribution cannot be made to a Roth IRA. Instead it must be made to a Traditional IRA. The tax-deferred growth is the primary benefit of the Traditional IRA for someone who does not receive any tax benefit for the contribution.

What are the rules for contributing to a traditional IRA?

Having earned income is a requirement for contributing to a traditional IRA, and your annual contributions to an IRA cannot exceed what you earned that year. Otherwise, the annual contribution limit is $6,000 in 2021 ($7,000 if age 50 or older).

What are the characteristics of a traditional IRA?

Traditional IRA Characteristics Contributions may be tax-deductible. Earnings grow tax-deferred. Distributions generally are taxable. Distributions before you reach age 59% are subject to penalty tax, unless you have an early distribution penalty tax exception.

What is a traditional IRA for tax purposes?

Traditional individual retirement accounts, or IRAs, are tax-deferred, meaning that you don’t have to pay tax on any interest or other gains the account earns until you withdrawal the money. The contributions you make to the account may entitle you to a tax deduction each year.

When can you not contribute to an IRA?

For 2020 and later, there is no age limit on making regular contributions to traditional or Roth IRAs. For 2019, if you’re 70 ½ or older, you can’t make a regular contribution to a traditional IRA.

Do I have to report IRA contributions on my tax return?

Traditional IRA contributions should appear on your taxes in one form or another. If you’re eligible to deduct them, report the amount as a traditional IRA deduction on Form 1040 or Form 1040A. Roth IRA contributions, on the other hand, do not appear on your tax return.

What are the 3 types of IRA?

Types of IRAs include traditional IRAs, Roth IRAs, SEP IRAs, and SIMPLE IRAs. If you withdraw money from an IRA before age 59½, you are usually subject to an early withdrawal penalty of 10%. There are income limitations for contributing to Roth IRAs and for deducting contributions to traditional IRAs.

Is the income from a traditional IRA taxable?

Qualifying distributions from traditional IRAs are nontaxable while qualifying distributions from Roth IRAs are fully taxable as ordinary income. FALSE – just the opposite is true. Qualifying distributions from Roth IRAs are nontaxable while qualifying distributions from traditional IRAs are fully taxable as ordinary income.

When to roll over a traditional IRA to another IRA?

A rollover from a Traditional IRA to another IRA MUST be done within ___ days to avoid tax consequences. Which of these statements concerning Traditional IRAs is CORRECT? Which of the following employers is required to follow ERISA regulations?

Which is the following statement regarding Roth 401k accounts is false?

Which of the following statements regarding Roth 401 (k) accounts is false? A. Employees can make contributions to a Roth 401 (k). B. Employers can make contributions to Roth accounts on behalf of their employees. C. Contributions to Roth 401 (k) plans are not deductible.

How old do you have to be to receive distributions from an IRA?

Erica is 35 years old and owns an IRA. At what age can she begin to receive distributions without a tax penalty? A rollover from a Traditional IRA to another IRA MUST be done within ___ days to avoid tax consequences. Which of these statements concerning Traditional IRAs is CORRECT?