Who can receive income from a charitable remainder trust?

You or your chosen beneficiaries receive an income stream Based on how you set up the trust, you or your stated beneficiaries can receive income annually, semi-annually, quarterly or monthly. Per the IRS, the annual annuity must be at least 5% but no more than 50% of the trust’s assets.

How is income from charitable remainder trust taxed?

First, the payment is taxed as ordinary income to the extent of the CRT’s ordinary income for that year and undistributed ordinary income from prior years. Second, the distribution is treated as capital gains to the extent of the CRT’s capital gains for that year and undistributed capital gains from prior years.

Does a charitable remainder trust file a tax return?

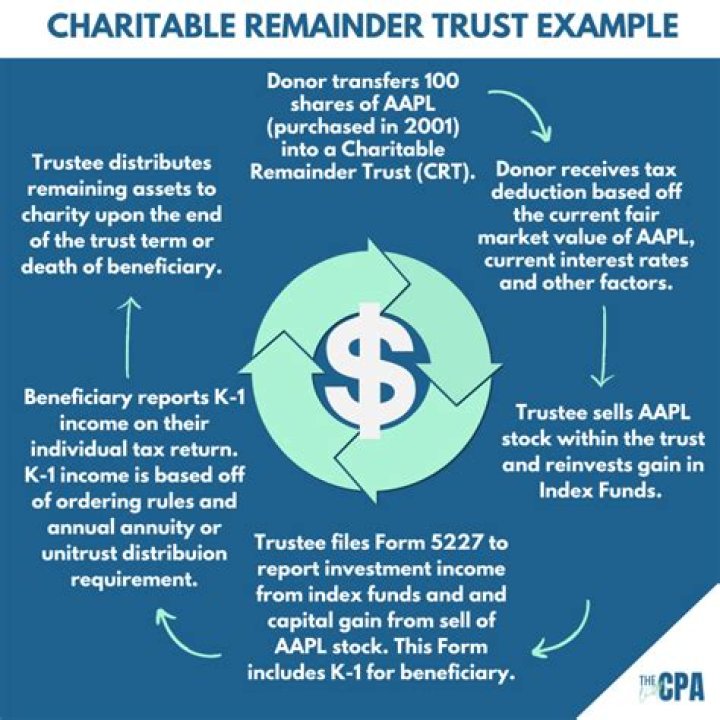

The trust is required to file federal and state fiduciary income tax returns if the trust has a certain amount of income during a taxable year. Because a charitable remainder trust is ordinarily tax-exempt, the trust will calculate net income at the trust level, but will pay no tax.

What are the rules for a Charitable Remainder Trust?

Per the IRS, the annual annuity must be at least 5% but no more than 50% of the trust’s assets. 3. After the specified timespan or the death of the last income beneficiary, the remaining CRT assets are distributed to the designated charitable beneficiaries.

What happens to the assets of a charitable trust?

the remaining trust assets upon termination. Charitable remainder trusts can be either annuity trusts or unitrusts, depending on the method used to calculate the payment amounts.

Can a charitable trust be used for tax deductions?

Not all trusts that are created for charities qualify for the estate tax charitable deduction. The estate of a donor is entitled to a charitable deduction if—and only if—the trust is a charitable remainder unitrust or a charitable remainder annuity trust.

Do you have to pay taxes on the remainder of a trust?

You can expect to pay an additional $500 to $2,000 or sometimes more every year for the remainder of the beneficiary’s life, to maintain the trust from a legal and tax compliance standpoint. You not only need to file a special CRUT tax return, but you also must file a K-1 with the beneficiary which complicates his return.