Who can sign an 1120 tax return?

The CCA relies upon Section 6062, which provides that corporate returns must be signed by the “president, vice-president, treasurer, assistant treasurer, chief accounting officer or any other officer duly authorized.” This is repeated in the Form 1120 instructions under “Who Must Sign,” where it says “the president.

Can a former officer sign a tax return?

Any corporate officer can sign, provided the corporation authorizes him to do so. The individual must be a corporate officer, such as a tax officer. An individual who is not an officer, such as a non-officer tax director, is not eligible to sign the return.

Can a director sign tax return?

Who can sign off a corporation tax return?

On this basis, you should accept the signature of any company official, employee or agent (including a tax advisor or an accountant). In addition, you may accept returns that are `signed’ in the name of a firm of accountants.

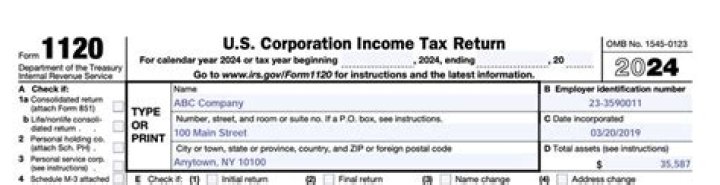

What do you need to know about Form 1120?

Corporations can generally electronically file (e-file) Form 1120, related forms, schedules, and attachments; Form 7004 (automatic extension of time to file); and Forms 940, 941, and 944 (employment tax returns). If there is a balance due, the corporation can authorize an electronic funds withdrawal while e-filing.

What are the limitations on charitable contributions on Form 1120?

Line 19. Charitable Contributions Limitation on deduction. Carryover. Suspension of 10% limitation for farmers and ranchers and certain Native Corporations. Temporary suspension of limitations on certain contributions. Temporary suspension of 10% limitation for certain disaster-related contributions. Cash contributions.

Can a single member LLC file a Form 1120?

Generally, a single-member LLC is disregarded as an entity separate from its owner and reports its income and deductions on its owner’s federal income tax return. The LLC can file a Form 1120 only if it has filed Form 8832 to elect to be treated as an association taxable as a corporation.

What should total receipts be for end of tax year?

If the corporation’s total receipts for the tax year and its total assets at the end of the tax year are less than $250,000, select Yes.