Who can use the accrual basis for accounting?

Accrual accounting is considered the standard accounting practice for most companies except for very small businesses and individuals. The Internal Revenue Service (IRS) allows qualifying small businesses (less than $25 million in annual revenues) to choose their preferred method.

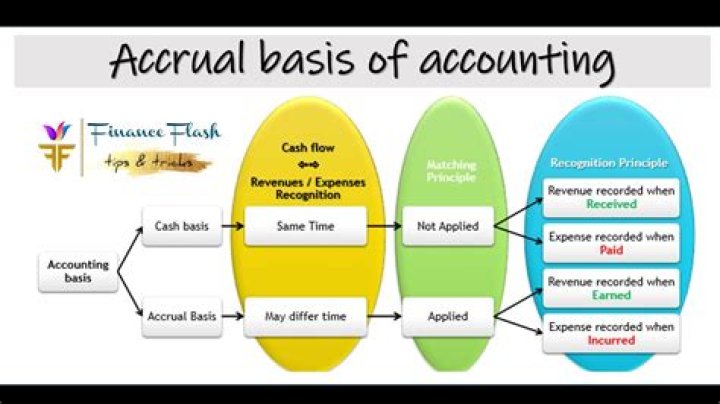

What is under the accrual basis of accounting?

Under the accrual basis of accounting, revenues and expenses are recorded as soon as transactions occur. This process runs counter to the cash basis of accounting, where transactions are reported only when cash actually changes hands.

Which is an example of accrual basis accounting?

In conclusion, cash basis accounting records revenue when cash is received from a customer and expenses are recorded when cash is paid to suppliers and employees. Accrual basis accounting records revenue when earned and expenses are recorded when consumed. What Is an Example of an Accrual?

How is accrual accounting used in the general ledger?

On the general ledger, when the bill is paid, the accounts payable account is debited and the cash account is credited. Accrual accounting is an accounting method where revenue or expenses are recorded when a transaction occurs rather than when payment is received or made.

When to report rent on the accrual basis of accounting?

Under the accrual basis of accounting I will report the rent expense in December because the rent was used up in December, and I will also report estimated utilities expense of $300 so that the December income statement provides a better measure of December’s profitability.

Why is accrual accounting not an accurate method of accounting?

Accrual accounting, however, says that the cash method is not accurate because it is likely, if not certain, that the company will receive the cash at some point in the future because the services have been provided.