Who is eligible for the qualified business income deduction?

Qualified Business Income Deduction Many owners of sole proprietorships, partnerships, S corporations and some trusts and estates may be eligible for a qualified business income (QBI) deduction – also called Section 199A – for tax years beginning after December 31, 2017.

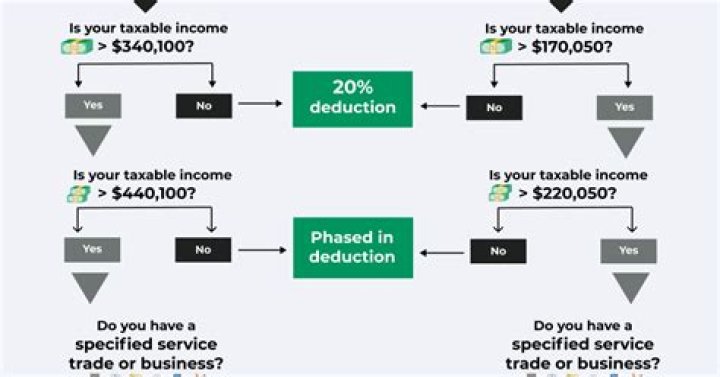

What’s the income limit for the 20% tax deduction?

For 2020, this applies if your taxable income is $326,600 to $426,600 if married filing jointly or $163,300 to $213,300 if single. In this event, only part of your deduction is subject to the W2 wage/property limit and the rest is based on 20% of your QBI. The phase-in range is $100,000 for marrieds, and $50,000 for singles.

What makes up qualified business income ( QBI )?

QBI is the net amount of qualified items of income, gain, deduction and loss from any qualified trade or business, including income from partnerships, S corporations, sole proprietorships, and certain trusts. Generally this includes, but is not limited to, the deductible part of self-employment tax, self-employed health insurance,…

When do you get the 20 percent tax break?

Generally, if you qualify for the deduction, the 20 percent break will apply to the lesser of your qualified business income or your taxable income minus capital gains. See below for an example from Levine of BluePrint Wealth Alliance. In this case, the taxable income of $118,500 is greater than the qualified business income of $100,000.

Is the C corporation eligible for the tax deduction?

Income earned through a C corporation or by providing services as an employee is not eligible for the deduction. For more information on what qualifies as a trade or business, see Determining your qualified trades or businesses in Publication 535.

When do you pay taxes on corporate income?

Minimum corporate income tax (MCIT) on gross income, beginning in the fourth taxable year following the year of commencement of business operations. MCIT is imposed where the CIT at 30% is less than 2% MCIT on gross income.