Who is the beneficiary of a variable annuity when the owner dies?

For most variable annuities, beneficiaries receive at least the original amount the owner contributed. For fixed annuities, the beneficiary receives the present value of payments. For some immediate annuities, such as a lifetime immediate income annuity without term certain, the insurance company keeps the money when the owner dies.

Do you have to pay taxes on an annuity when the beneficiary dies?

People inheriting an annuity owe income tax on the difference between the principal paid into the annuity and the value of the annuity at the annuitant’s death. If they choose a lump sum, beneficiaries must pay owed taxes immediately.

Can a younger representative be included in an annuity?

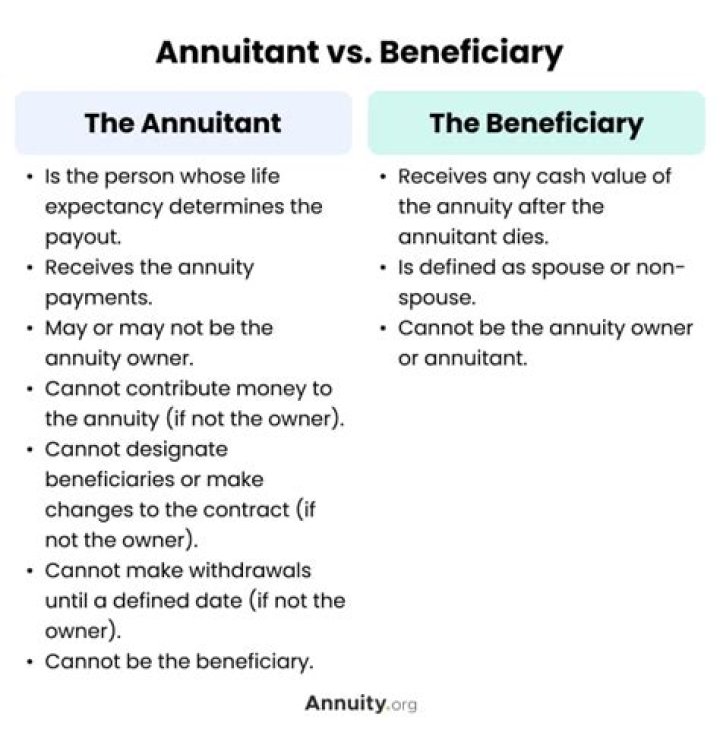

While finalizing terms of the annuity agreement, the owner has the option of including an annuitant. It is common for the annuity owner to name themselves as the annuitant. However, sometimes an annuity owner elects to name a younger representative as the annuitant to stretch out payments and extend the tax liability.

Can a beneficiary of an inherited annuity change their name?

Inherited annuities are taxable as income. The beneficiary of a tax-deferred annuity may choose from several payout options, which will determine how the income benefit will be taxed. If the beneficiary is the spouse of the annuitant, the spouse can change the contract into his or her own name.

What happens when an annuity reaches its maturity date?

There are different options when an annuity reaches its maturity date, but how that plays out has a lot to do with how the annuity was set up when it was started. Annuities are contracts between you and the insurance company, where the details – often including maturity options – are spelled out ahead of time.

What happens to the earnings of an inherited annuity?

The earnings on an inherited annuity are taxable. How inherited annuities are taxed depends on their payout structure and whether the one inheriting the annuity is the surviving spouse or someone else. What Happens to an Annuity When You Die?

How old do you have to be to get a longevity annuity?

This is a common concern, even among elderly who are well-to-do. Like all annuities, longevity annuities can be set up with various provisions. However, you typically must wait until you reach the age of 80 before receiving income distributions from the contract.

What do you need to know about a lifetime annuity?

Lifetime Annuity. A lifetime annuity is a financial product you can buy with a lump sum of money. In return, you will receive income for the rest of your life. A lifetime annuity guarantees payment of a predetermined amount for the rest of your life.

How does a deferred lifetime annuity work?

A Deferred Lifetime Annuity is where the payments start at a predetermined future date. With a Deferred Annuity the purchaser pays in over time (or one lump sum). The money is then invested by the insurance company.

How is inherited annuity income reported to the IRS?

Inherited annuity income should be reported to the Internal Revenue Service, as a general rule, the same way the plan participant would have reported it. There are exceptions to this, however. For example, a beneficiary may be entitled to an estate tax deduction if the annuitant died after the annuity starting state.

What happens to the money in an annuity after death?

An annuity is a financial instrument that accrues interest on a tax-deferred basis and protects against market risk ad longevity risk. Because annuities offer many benefits, lottery winners, retirees and structured settlement recipients use them to create predictable cash flow for the present, future and even after their death.

Do death benefits from an annuity become part of the estate?

Estates. If you leave your death benefits from an annuity to a nonspousal beneficiary, the amount becomes part of your gross estate valuation. Because it is left to a beneficiary, it might not pass through the probate process, but that does not mean the value of the annuity is not part of your estate valuation for tax purposes.

Who is the primary owner of an annuity?

owned by another party and payable to a trust. When an annuity is owned by a trust, the holder of the annuity is deemed by Section 72 (s) (6) (A) to be the primary annuitant. This provision applies to any annuity owned by an entity other than a natural person, including a corporation, partnership, or trust.

Can a surviving spouse be the joint owner of an annuity?

But that rule triggers based on whether the spouse is named as the beneficiary, not the joint owner. In fact, once a surviving spouse is properly named as a beneficiary, there’s often no reason at all for the annuity to be jointly owned anymore!

Are there any exceptions to the tax rules for immediate annuities?

Notable exceptions are contracts held in a trust or other entity as an agent for a natural person, immediate annuities, annuities acquired by an estate upon the death of the owner. Annuities are also not taxable if owned by a charitable organization or a pension plan.

How is the non taxable portion of an annuity determined?

During annuitization, a portion of each annuity payment represents a return of non-taxable investment in the contract and the balance of each payment is considered taxable income. The taxable and non-taxable portions of the payments are determined by an exclusion ratio.

Can a beneficiary of an inherited annuity use the money?

Yes. An inherited annuity can provide money for the beneficiary to pay off major expenses (such as student debt, a mortgage, health-care costs, etc.). If you decide to sell your inherited annuity, you can do so in one of three ways:

What happens to my parent’s annuity when I Die?

If your parent was receiving annuity payments, the policy generally no longer has a cash value. You may receive payments if your parent did not fully collect a guaranteed number or amount of payments. If your parent’s annuity had survivor benefits, you’ll receive payments for a set period or for the rest of your life.

When does a minor become a beneficiary of an annuity?

A minor designated as the beneficiary of an annuity can access the inherited funds only when he reaches the age of 18. The beneficiary may then choose whether to receive a lump-sum payment. 4. Other beneficiaries

What are the different types of fixed annuities?

Fixed annuities can be either immediate (meaning they provide fixed payouts, determined by annuity size and annuitant’s age, almost immediately following the accumulation phase) – or deferred (which means they continue to collect interest at a set rate and payouts are made later).

What are the tax benefits of a deferred annuity?

A deferred annuity receives pre-tax contributions. The income derived from the annuity is only taxed upon withdrawal. It enables the annuitant to defer paying taxes on the earnings from the annuity almost indefinitely. Deferred annuities offer the annuitant several options for receiving distributions.