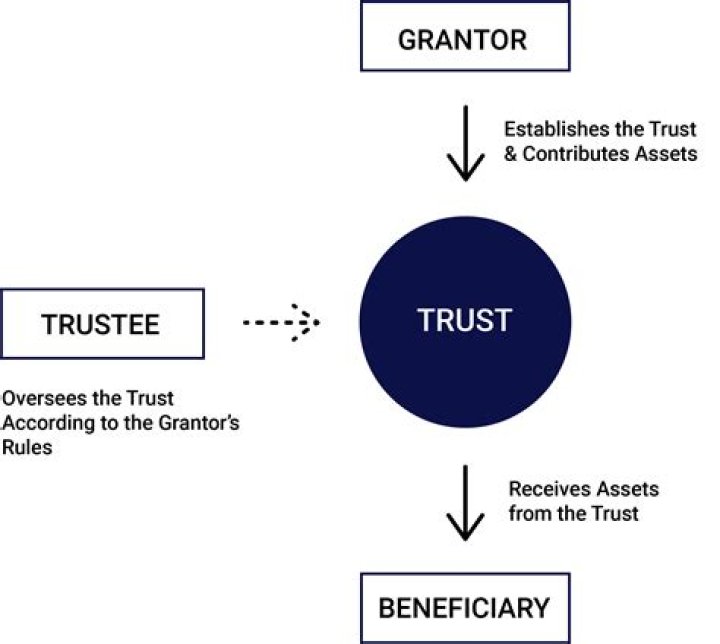

Who is the grantor of a revocable trust?

A Grantor creates a Trust. He or she is the legal and rightful owner of all property and assets that will be put into that Trust. While in real estate, the term “Grantor” is used to signify a property seller, when we’re talking about Estate Planning, the grantor definition is the entity creating a Trust.

Is a revocable trust considered a grantor trust?

A grantor trust is a trust in which the individual who creates the trust is the owner of the assets and property for income and estate tax purposes. All grantor trusts are revocable living trusts, while the grantor is alive.

What is the difference between a grantor trust and a complex trust?

Complex trusts may accumulate income, distribute amounts other than current income and, make deductible payments for charitable purposes under section 642(c) of the Code. A grantor trust is a trust over which the grantor has retained certain interests or control.

How do you end a revocable trust?

If you’re terminating the trust because the principal is so low that maintaining the trust administration is no longer reasonable, you’ll need to file a petition with the probate court for termination.

A grantor trust is a trust in which the individual who creates the trust is the owner of the assets and property for income and estate tax purposes. Grantor trust rules are the rules that apply to different types of trusts. All grantor trusts are revocable living trusts, while the grantor is alive.

A “grantor trust” can, in a given case, be either revocable or irrevocable, although most types of “grantor trusts” involve an irrevocable trust. Certain types of trusts (such, as for example, a revocable trust) are disregarded not only for income tax purposes but also for federal estate and gift tax purposes.

What happens to a grantor trust when the grantor dies?

In the year the grantor dies, the trust continues to report in the same manner previously used before the grantor died. Under the traditional method of tax reporting, the trustee would be required to file a fiduciary tax return for the trust tax year that ends with the decedent’s date of death.

Can a grantor trust be held by an independent trustee?

IRC §674(c) enumerates powers that will not trigger grantor trust status if they are held by an independent trustee. An independent trustee may be given fairly broad powers over beneficial enjoyment without causing the grantor to be treated as the owner.

Can a spouse circumvent the grantor trust rules?

For the purpose of the grantor trust rules, the grantor of a trust is treated as owning any powers or interests held by his or her spouse. Accordingly, a grantor cannot circumvent the grantor trust rules by having prohibited powers or interests held by the grantor’s spouse.

When was the grantor trust rule first created?

The grantor trust rules were first developed in the late 1960s in order to thwart taxpayers’ use of trusts to shift income into lower tax brackets.