Who Must File NJ partnership return?

Every partnership that has income or loss derived from sources in the State of New Jersey, or has any type of New Jersey resident partner, must file Form NJ-1065. A partnership must file even if its principal place of busi- ness is outside the State of New Jersey.

Do trusts need to file a tax return?

Q: Do trusts have a requirement to file federal income tax returns? A: Trusts must file a Form 1041, U.S. Income Tax Return for Estates and Trusts, for each taxable year where the trust has $600 in income or the trust has a non-resident alien as a beneficiary.

What is NJ 1065e?

2002. STATE OF NEW JERSEY – NONRESIDENT PARTNER’S. STATEMENT OF BEING AN EXEMPT CORPORATION OR MAINTAINING A. REGULAR PLACE OF BUSINESS IN NEW JERSEY.

What does physical nexus to NJ mean?

New Jersey Tax Nexus Generally, a business has nexus in New Jersey when it has a physical presence there, such as a retail store, warehouse, inventory, or the regular presence of traveling salespeople or representatives.

How is NJ allocation factor calculated?

Section 18:7-8.7 – Business allocation factor; determination or receipts fraction (a) The percentage of the taxpayer’s receipts within New Jersey is determined by ascertaining the taxpayer’s receipts allocable to New Jersey during the period covered by the return and dividing the sum of the receipts by the taxpayer’s …

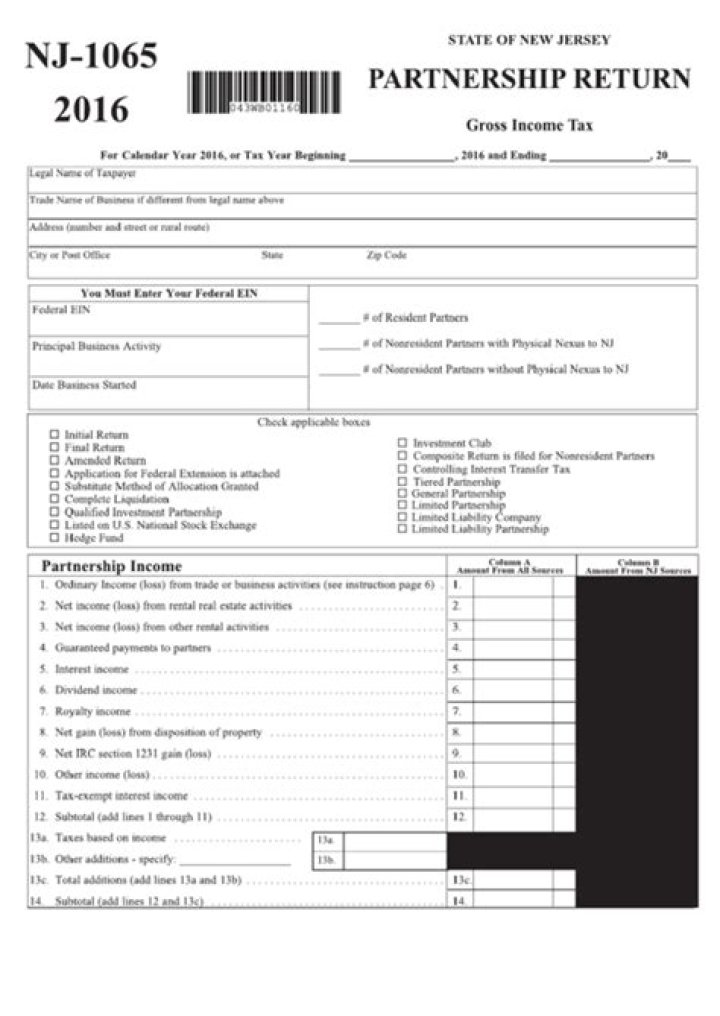

What is nj1065?

2020. New Jersey Partnership Return. Gross Income Tax. For Calendar Year 2020, or Tax Year Beginning.

Who is subject to the NJ partnership filing fee?

Most entities classified as partnerships for federal income tax purposes that have income or loss derived from New Jersey sources and that have more than two owners shall make a payment of a filing fee of $150 for each owner up to a maximum of $250,000.

What is NJ partnership filing fee?

$150

Partnerships compute and report the filing fee on Form NJ-1065. payment penalties and interest for the filing fee. Partnerships must pay $150 for each individual, trust, estate, or entity, including any “pass- through” entity that owns a partnership interest, up to a maximum of $250,000.

How do I amend my NJ tax return 2019?

If you need to change or amend an accepted New Jersey State Income Tax Return for the current or previous Tax Year, you need to complete Form NJ-1040X (residents) or Form NJ-1040NR (nonresidents and part-year residents). Forms NJ-1040X and NJ-1040NR are Forms used for the Tax Amendment.

Does New Jersey tax partnerships?

Partnership determines the tax for the nonresident corporate partners at the 9% corporate rate, unless they maintain a regular place of business in New Jersey or they are an exempt corporation (N.J.S.A. 54:10A-3).

How to file a partnership in New Jersey?

In addition, the partnership must pay one-half of the filing fee for the tax year as the prepayment towards the filing fee for the next tax year. NJ-1065 filers that have ten or more partners are required to file by electronic means. For partnerships with 50 partners or less, the Division provides a free online partnership filing application.

Can a PTE be a New Jersey combined group?

If all the members of the PTE are taxpayers otherwise liable for New Jersey gross income tax, and no entity subject to the New Jersey corporation business tax (CBT) has a direct, indirect, beneficial, or constructive ownership or control of the PTE, then the PTE cannot be a member of a New Jersey combined group.

What is the elective entity tax in New Jersey?

The distributive proceeds (sourced to New Jersey) are allocated $450,000 to Member A and $450,000 to Member B. Tax is imposed on the sum of each member’s share of distributive proceeds, which is $900,000. The elective entity tax is $56,567.50.

How are pass through entities taxed in New Jersey?

Example 3: Pass-through entity ABC has 3 New Jersey resident members with total income of $500,000 that is 40% sourced to New Jersey resulting in New Jersey sourced income of $200,000. The distributive proceeds (sourced to New Jersey) are allocated $100,000 to Member A, $60,000 to Member B and $40,000 to Member C.